Zoom: More than video?

After a 420% stock price growth in 2020, Zoom lost it all and came back to where it was before the COVID-19 pandemic. Today I will describe Zoom to see if it’s still an attractive stock.

Cathie Wood still holds Zoom as a meaningful position in her ETF, as it is her 7th biggest as I write this article. So let’s get into it:

1. Company overview

Zoom is a market-leader in the video conferencing space. It sells its proprietary video-first software that includes a suite of complementary services aimed at improving the way people communicate for both commercial and personal usage.

The cornerstone of the platform is Zoom Meetings, around which the company provides a full suite of products and features designed to give users an easy, reliable, and innovative unified communications experience.

2. Product overview

Zoom product suite

- Zoom Meetings: Zoom Meetings provide HD video, voice, chat, and content sharing across mobile devices, desktops, laptops, telephones, and conference room systems.

This is Zoom’s flagship product (“cash cow”) that the company looks to constantly improve in order to maintain a high customer satisfaction and attract new business.

- Zoom Chat – It is included in the Zoom client for meeting and phone customers, enables organizations and teams to communicate and collaborate in groups, channels, or 1-1s and to stay connected by instantly sharing messages, images, audio files, and other content across desktop, laptop, tablet, and mobile devices.

- Zoom Rooms - Zoom Rooms is a software-based conference room system that transforms every room–from executive offices, huddle rooms, training rooms into a collaboration space that is easy to manage while using the conference room audiovisual (AV) equipment.

- Zoom Phone - an enterprise cloud phone system that provides powerful private branch exchange (“PBX”) features, such as secure call routing, call queuing, call detail reports, call recording, call quality monitoring, voicemail, switch to video, and much more. It’s like a phone call, on steroids. It can be used across both laptops and traditional phones.

- Zoom Video Webinars - support interactive video presentations to large audiences from almost anywhere in the world and from many devices. Zoom webinars scale up to 50,000 people including up to 100 interactive video panelists.

3. Business model

3.1 Revenue – How does the company make money?

Zoom generates revenue from the sale of subscriptions for their unified communications platform. Subscription revenue is driven primarily by the number of paid hosts as well as purchases of additional products.

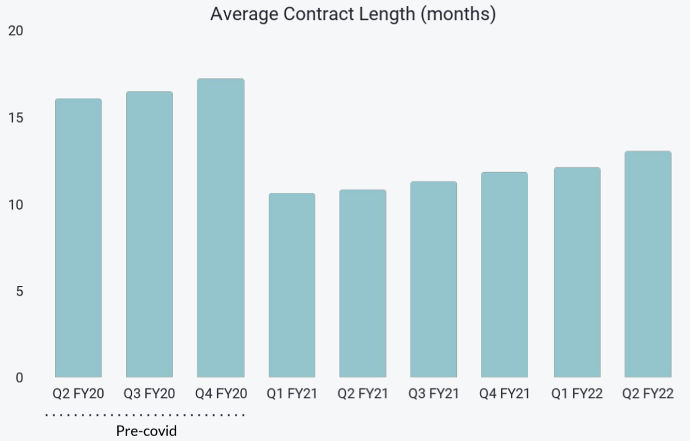

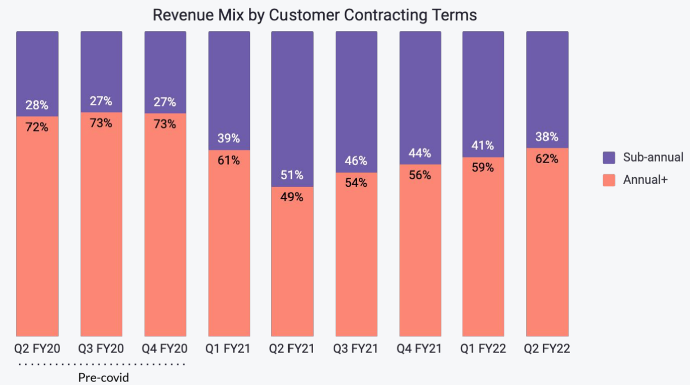

Revenue visibility offered by high % of recurring revenue

As we can see, Zoom is used to signing long-term contracts with customers, that will offer better revenue visibility for the company. The last quarters showcased an improvement in the trend, but remain significantly below the pre-pandemic trend.

Moreover, 62% of Zoom’s customers are signing annual contracts, which is another + for the company.

In terms of customer concentration risk, no customer represents more than 10% of the company’s revenue.

Customers categories

Zoom characterizes its customers into 3 groups:

- customers < 10 employees

- customers > 10 employees:

- customers with more than $100k in TTM revenue:

Starting with the 4th quarter of 2021, Zoom has changed one important metric that it used to assess its performance. Instead of focusing on customers based on their size (< or > 10 employees), the company will focus on the way the customers have been engaged.

Enterprise Customers refers to customers who have been engaged by Zoom’s direct sales team, channel partners, or independent software vendor (ISV) partners. All other customers are referred to as Online Customers.

Zoom NPS

In September 2021 Zoom had its annual analyst day, where the company revealed a Net promoter score (NPS) above 70. The metric is used for evaluating customer experience and measures the loyalty that customers showcase towards a company.

Usually, a NPS bigger than 70 means that a company is doing a great job (https://www.retently.com/blog/turn-advocates-feedback-reviews/ ) and customers are very pleased with the way things are going. This might generate customer referrals that will make it easier to attract new customers.

3.2 KPIs

Nr of customers

At the end of 2021 the >10 employees category represented around 67% of its revenue.

Customers with more than $100k spent in the last 12 months represent around 23% of Zoom’s revenue.

At the end of 2021, there were around 191k Enterprise customers, representing 50% of the revenue.

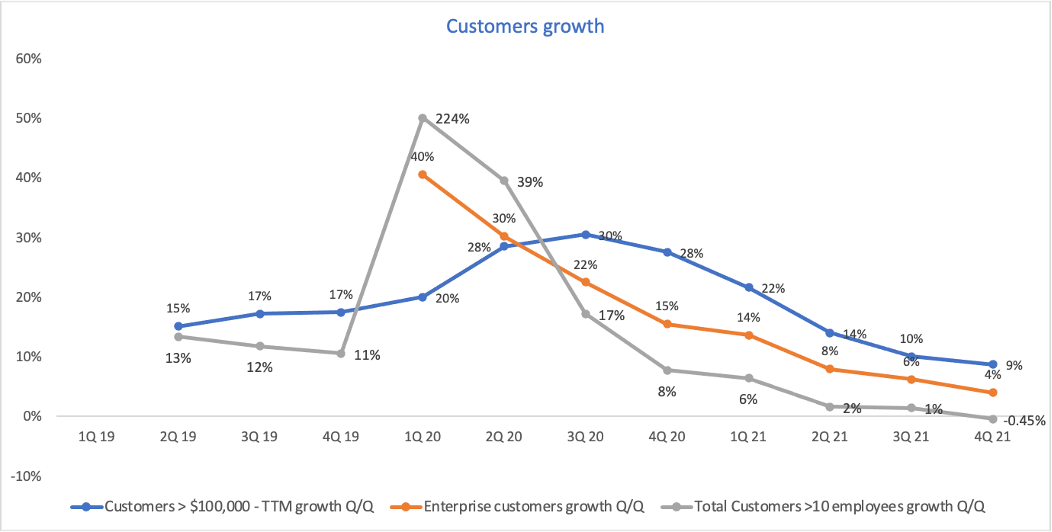

Customers growth

Customers > 10 employees – the number of customers decreased at the end of 2021 compared with Q3 2021. The company doesn’t disclose a churn rate, but instead it chose to focus on the Enterprise customers.

Enterprise customers grew modestly in the last quarters, coming in with only a 4% growth quarter over quarter.

Customers with over $100k in annual spending grew 9% Q/Q at the end of 2021.

As a conclusion, we can see the immense spike in the first quarter of 2020 when the COVID-19 pandemic hit. As a result, Zoom benefited from both organic and inorganic customers growth. Going forward, the company will allocate more resources on the preferred segment of customers in order to keep attracting new potential customers and expand.

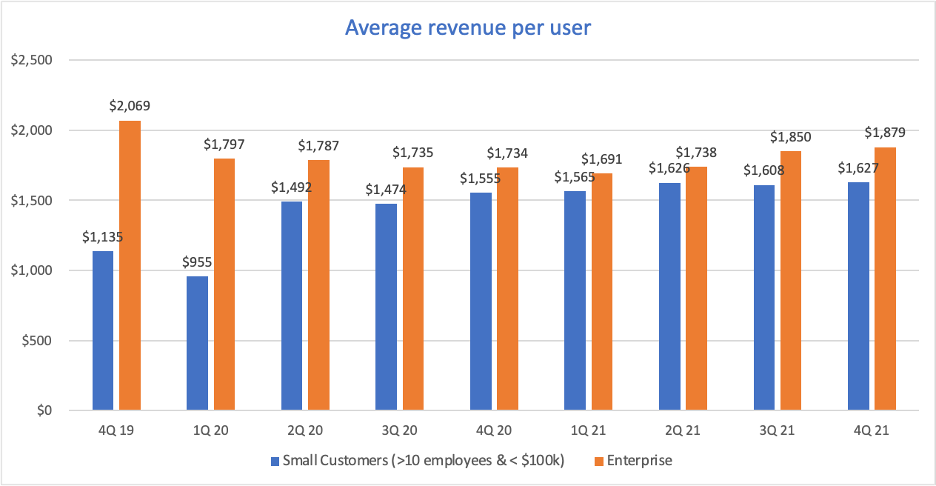

Average revenue per user

As we can see above, the average quarterly spending for the Enterprise customers has been consistently higher than the customers with more than 10 employees, but with a lower spending that $100k annually.

Net Dollar Expansion Rate TTM

The TTM Net Dollar expansion Rate is a measure that shows how much more does a customer spends on the Zoom platform as compared to 12 months ago. It includes any upsell or expansion from a customer.

Zoom just started reporting this metric for both Enterprise and >10 employees customers.

For its Enterprise customers, the Net dollar expansion rate has been consistently bigger than 130%. In its last quarter it was just at 130%, which is a great value for a software company.

For the > 10 employees customers, it just recorded a 129% value, after being higher than 130% for 14 consecutive quarters.

This is a great metric that showcases how well the company can monetize its existing customers.

However, the level of penetration for additional services is very low for Zoom:

- 5% Zoom Rooms Account penetration (for >10 employees customers)

- 4% Zoom Phone Account penetration (for >10 employees customers)

This means that usually the existing customers are embarking more employees to the Zoom platform, which leaves a ton of room for Zoom to upsell its adjacent products.

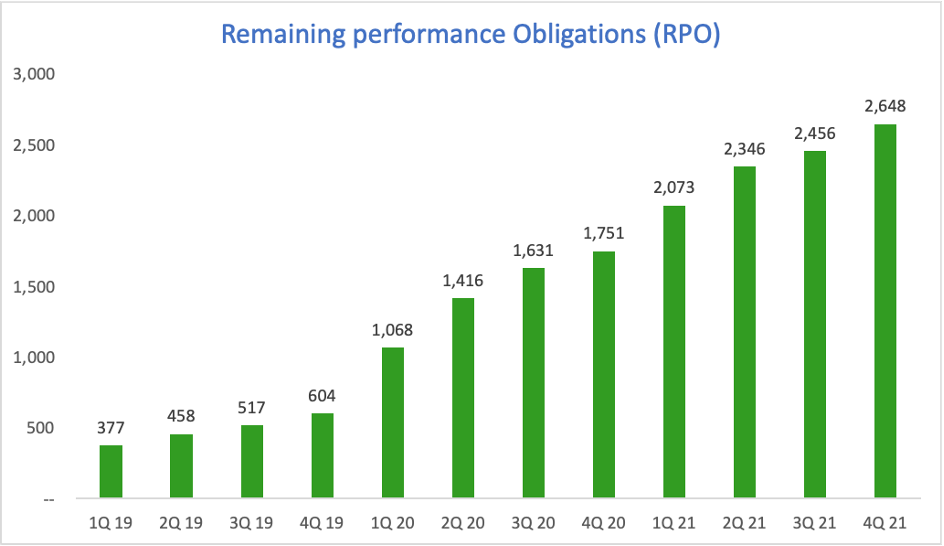

Remaining Performance Obligation (RPO)

Remaining performance Obligations (RPO) consists of both billed considerations and unbilled amounts that Zoom expects to recognize as revenue.

RPO shows how much Zoom’s customers have committed to spend on the platform. It is the sum of deferred revenue (billed, unearned revenue) and backlog (future performance obligations that haven't been invoiced).

RPO = deferred revenue (billed, unearned revenue) + backlog (future performance obligations that haven't been invoiced)

Zoom expects to recognize 67% of the RPO as revenue in the next 12 months and 37% later than 12 months as of 31 January 2022.

Customer Acquisition Cost (CAC)

This metric shows how well the company is using its sales&marketing team. It’s important to analyze sales efficiency to ensure that growth is efficient and sustainable.

Unfortunately, for Zoom, for its Enterprise clients (customers that have been engaged by Zoom’s direct sales team) the CAC went through the roof. As we can see, less and less customers have been added in 2021 on a Quarter/Quarter basis while the S&M expenses have growth consistently.

As a result, the CAC is very high and it seems like Zoom has temporary difficulties intro attaining new customers. As a result of the high CAC, the lifetime value for the new customers is very low and it is generally lower than the cost of attaining a new customer.

CAC Payback period

This shows how many years it takes on average for a customer to produce enough gross profit to pay back its CAC.

As we can see here, as a result of the increase in the customer acquisition cost, the CAC payback period has seen a tremendous increase. This means it would take an average enterprise customer around 7 years to generate enough gross profit to compensate for the cost of acquiring the customer. The trend is definitely deteriorating and Zoom must find ways to attract new customers at a lower rate. The last S&M budget spent in Q4 2021 is not included here, although the S&M spending grew with 52% as compared to Q4 2020.

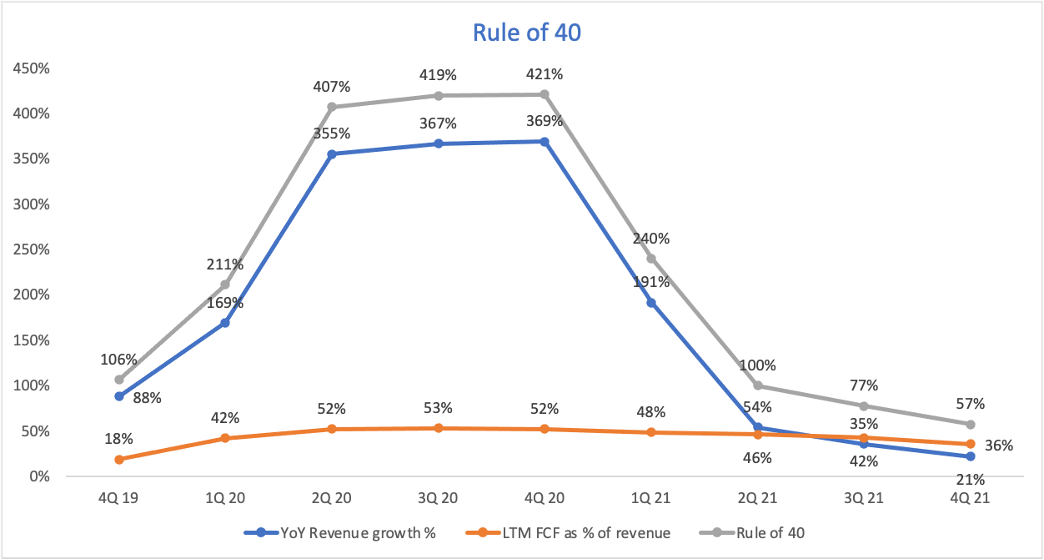

Rule of 40

Rule of 40 is another crucial metric for the health of any software business. It’s compiled of two crucial operating metrics:

- YoY revenue growth %

- Free cash flow as % of revenue for the last 12 months

As we can see, Zoom grew its revenues tremendously in the first quarter of 2020 as a result of the COVID-19 pandemic. Because of the abnormal revenue growth in 2020, for 2021 the growth has obviously slowed down, with the revenue growing in Q4 2021 with only 21%.

However, the company has consistently maintained a high free cash flow % as compared to the revenue. If before the pandemic the free cash flow was only around 18%, now it sits around 36%. This has been a great aspect for Zoom in the last two years as the company managed to transform most of its revenue into free cash flow.

As a conclusion, the rule of 40 remains a plus for Zoom since the company has a result of 57% in Q4 of 2021, but it needs to be followed closely in the subsequent periods.

To summarize the KPIs section, the sales efficiency metrics have deteriorated and the momentum gained in 2020 has definitely slowed down. Zoom is now in a position where it is forced to upsell its new offerings to existing customers. That will translate to a high NRR, so watch for this metric in order to see how the company does.

The good news is that Zoom is now in a position with a lot of flexibility. It has no debt on the balance sheet, a tremendous cash position, it is free cash flow positive and has a cohort of customers that love the platform and are committed to spend more here.

3.3 Capital allocation – is Zoom’s management allocating capital well?

One metric that can help paint a picture is the Return on Invested capital (ROIC):

The reason why we calculate the return on invested capital is to compare it with the cost of capital (WACC). If a company has ROIC > WACC, the company creates value for its shareholders.

You can read more about it on the 1$ test explained by Warren Buffet.

ROIC > WACC -> Value created

Going further down a level, ROIC can be also expressed as a function of:

What this analysis does is it tells us if the company has increased its net operating profit margin or if the return is better just because the company sold more units per 1$ invested (bigger sales turnover).

For Zoom here’s how ROIC looks like:

As we can see, the ROIC grew exponentially starting with 2020. This came as a result of both a better profit per sale (higher Nopat/Sales ratio) as well as a high number of sales for the same 1$ of invested capital.

However, if we’re going the analyze the trend of the two in conjunction, we can see that most recently the operating profit margin has increased drastically while the contribution of the sales turnover has decreased.

To conclude, the low NOPAT margin from 2019 is explained by the growth nature of Zoom and the company has improved its NOPAT margin immensely during the last two years.

This translated into a significant return on invested capital, much bigger than an average cost of capital for a SaaS business (usually lower than 10%). Zoom has captured successfully the tailwind that the COVID-19 pandemic created in its industry.

For the calculation I used 2 assumptions:

- The tax rate I used is 17.2%, which is the highest tax rate Zoom paid in any quarter. The company still benefited from net loss deduction and didn’t pay any taxes in most of the quarters analyzed.

- Zoom holds a lot of cash on its balance sheet. I did not remove the excess cash when I calculated the Invested Capital.

3.4 Growth opportunities

Zoom’s growth strategy is easy: Double down on the enterprise growth strategy. Then every 1-2 year add a new service and upsell.

This model has been accelerated because of the pandemic and the company was forced to launch new products faster than in a normal environment. However, it coped well with the market and showcased flexibility in new more products to meet its customers’ needs.

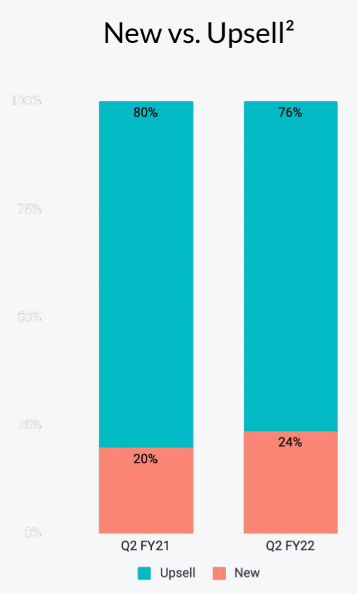

Upsell opportunities

These stats are only for customers with more than 10 employees.

For now, Zoom’s revenue comes mostly from the Zoom Meetings. I think the penetration level for the additional products sold by the company is very low and Zoom might be struggling to upsell customers.

On the flip side, since there are many existing customers, Zoom doesn’t have to spend money to attract new ones. They only need to gradually attract the customers to their platform while they meet their needs.

“We are going to target those customers who really want to standardize on Zoom platform, probably start from Meeting. And for those customers who deploy both Meeting and Phone, now they look at the Contact Center.” – Zoom CEO, February 2022

Zoom Phone

Zoom has reported surpassing the 2 million paid seats mark for Zoom Phone in September 2021. In the last earnings call, Zoom’s CFO said that the company added 550 thousand new paid seats for Zoom Phone, which translates into over 2.5 million paid seats at the end of January 2022.

The company launched the service in January 2019 and in just two and a half years it has been able to become a significant player in the space. The pandemic tailwinds might of have an impact but the results are still remarkable.

Most of the seats came from customers that are already using the Zoom Meetings:

Stepping into the UCaaS land

Unified Communications as a Service (UCaaS) integrates many communications avenues, such as phone, chat, and video conferencing. It enhances productivity and provides ways to interact across different communication channels.

UCaaS has proven itself as the most resilient and cost-efficient enterprise communication service. Companies no longer have to run analog phone lines to every person to talk or work on projects. It also operates in the cloud, which withstands natural disasters.

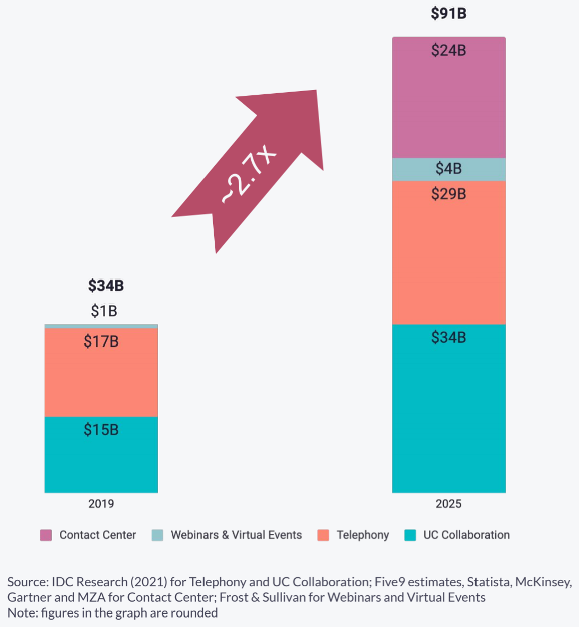

During the last couple of years, Zoom added Rooms, Phone and Events as a way to enhance its offer. As a long-term play, Zoom just entered the Contact Center market with its internally developed Zoom Contact Center.

Zoom Contact Center can be thought of as a specialized customer-care tool that combines unified communications and contact center capabilities with the useability of the Zoom platform. Zoom Contact Center supports customer service use cases and workflows using channels like video and voice, with SMS and webchat.

With this move, Zoom definitively enters the Contact Center as a Service (CCaaS) business, which is usually an important part of a Unified Communications offering.

The total addressable market is huge in this space, as shown below. The study estimates a phenomenal 25% CAGR between 2021 and 2025:

")

Within the Americas, North America shows the most pronounced growth. North America is currently the largest UCaaS market by revenue and the second in users.

IDC classified the leaders in the UC&C market by total revenue in 2020. As of then, the market leader was Microsoft with around $16.1 billions in revenue, representing a 34% market share.

Cisco came in second with a revenue of $5 billion, around 10.5% of the market. Zoom came in third with a revenue of $2.6 billion and a market share of around 5.5%.

As of now, Zoom’s offering in the field is very limited (almost of its revenue comes from Zoom Meetings) as the company is in the middle of a multiyear expanding strategy.

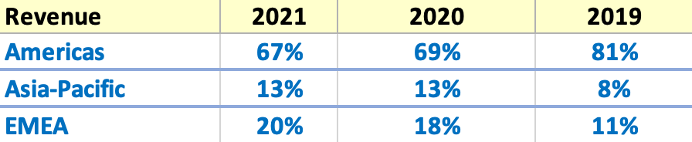

International expansion

Zoom made good progress in terms of international expansion, with the North America area representing only 67% of revenue at the end of 2021 as opposed to 81% at the end of 2019. The company made international expansion as a key growth driver for the future.

4. Management team

Zoom is a founder-led company. Its CEO and founder is Eric Yuan and he owns around 10% of the company. Together the management team owns around 20% of the company. I think that’s a great attribute for any investment. As long as the founder is still involved and has “skin in the game” that’s encouraging.

Zoom has done a tremendous job on delivering on their earnings estimate. In terms of revenue, the company didn’t miss any guidance in the last couple of years:

The same trend applies for the earnings. As we can see below, the management has been consistent on its promises, which is a great sign for any company.

I would say that the management team is a big plus for the company and it shows that the company has good leadership as it takes on the ferocious competition.

5. Industry Overview

Zoom acknowledges that its Total Addresable market (TMA) is limited in regards to the webinars&video events. Zoom must become a strong player in the internet telephony & UC collaborations in order to thrive.

Video Conferencing market

The video conferencing market is expected to grow from around $9.7 billion to around $22 billion by 2026, growing at a CAGR of around 17.8% according to Researchandmarkets.

Meticulous Research forecasts a similar path for the video conferencing industry. It estimates a growth from around $9 billion in 2021 to around $24.4 billion in 2028. This translates into a CAGR of around 15.5%.

Global video conferencing market share

A study published in October 2021 by Garner shows the market landscape for meetings solution. It has Cisco, Microsoft and Zoom as the market leaders in what is a very competitive space with many challengers:

As a summary of the 3 companies:

Cisco – offers its Webex Suite that is perceived as secure and reliable, has new features and specialized solutions added constantly and keeps the innovation going.

Microsoft – offers a unified client experience for meetings and office collaboration with Microsoft 365 suite that is cost-effective while keeps adding new capabilities at a rapid pace.

Zoom – offers a frictionless, video-first approach that is extremely easy to use and deploy that has generated great market traction as a result.

A study carried in March 2021 showed that Zoom is the most popular video conferencing platform in the world, dominating the market in 44 countries. On the second place we have Microsoft Teams with 41 countries and Google Meets with 21.

Zoom has around 300 million daily meeting participants. Microsoft teams is reported to have only around 145 million daily users in June 2021.

In the US, Zoom is the undisputed leader, with 60% of the market, followed by Google Meet with 12%.

Barriers to entry

The video communication space has low barriers to entry. With the recent technologic improvements, the service became very affordable, as we’ve seen entry prices as low as $4 / license for a month of usage (Microsoft’s newest offering).

Switching costs

The video conferencing solutions are sticky from a contractual stance. The contracts for enterprises are usually signed for long-term periods and it might be difficult to attract new customers. However, the apps are now very intuitive and it is very easy to switch providers as it doesn’t require any training for the employees.

De pus meme cu copilul care foloseste PCul!

Pricing power

This is a tricky one. Zoom has proved that cost isn’t necessarily the most important criteria for businesses when choosing a video service provider. As most of the companies are already using the Microsoft Office suite (around 48% of the office productivity market is owned by Office - I am honestly surprised that Microsoft Teams doesn’t dominate this space.

But Zoom’s user interface and ease of using are two things that made the company gain market share. Moreover, since Zoom is a customer-centered company (demonstrated by its high NPS score), it looks like the company has some pricing power.

5.1 Existing trends

WFH is here to stay

One study done one more than 30 000 US employees done in April 2021 showed that people that will be able to work remotely at least one day per week will we on average 4.8% more productive.

“The main source of this productivity boost is the savings in commuting time afforded by more WFH.”

The same study shows that on average, 20% of full working days will be carried remotely, as compared to only 5% before the pandemic hit, as a result of mainly better-than-expected WFH performance.

“Our data say that 20 percent of full workdays will be supplied from home after the pandemic ends, compared with just 5 percent before.”

Another study done in September 2021 by Owl Labs interviewed over 2000 US full-time workers revealed that:

84% of respondents also shared that working remotely after the pandemic would make them happier, with many even willing to take a pay cut.

Of those that worked from home during the pandemic, 70% of employees say virtual meetings are less stressful

70% of respondents want a hybrid or remote working style after the pandemic is over

Additionally, a study carried on 10 000 “white-collar workers” (workers in finance, technology, and energy) showed that 86% of them want permanent hybrid workweek or they will quit. To compromise, they would entertain a workweek with at least 2 days working remotely.

Another study done by the University of Chicago and Stanford University between April and September 2021 on more than 40 000 US workers showed:

- Employers are planning to offer an average of 2.15 days per week for WFH for employees able to work from home.

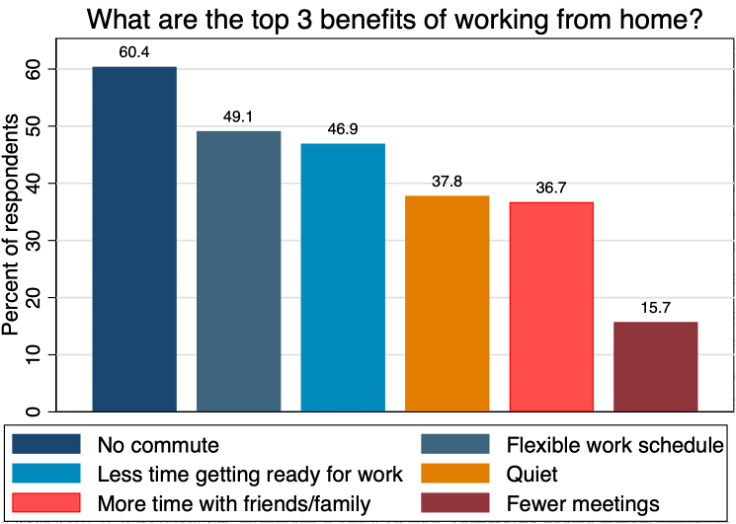

The top 3 reasons why people prefer working from home are:

- No commute (60%), flexible work schedule (50%), less time getting ready for work (47%), Quiet (38%) and more time spent with family (37%).

6. Competition

The video conferencing space is, as you can expect, very crowded. Some of the biggest competitors for Zoom are Microsoft’s Teams and Google Meet. Additionally, Cisco WebEx and GoToMeeting are also big players in the space.

Pricing

Microsoft offers its Teams service alongside the Microsoft Office package. The company has rebranded its flagship enterprise product from Microsoft Office to Microsoft 365 in order to also offer Teams.

The enterprise option that includes desktop versions of all the apps costs $12.5 /user with an enhanced offering for $22/user.

Additionally, Microsoft has recently launched a stand-alone version of Microsoft Teams aimed for small business. This “Teams Essentials” offers the basic features for the video-conferencing and starts at only $4/license. This aims to snatch some of that <10 employees market share from Zoom.

Zoom

Zoom’s meetings product starts from $15 for small companies and $20 dollars for enterprises with >10 employees.

The company also offers bundled packages that include Meetings, Chat and Phone. It can all be acquired for around $35 per license, paid annually.

Google Meet

Google Meet starts from $8 dollars and can cost up to $18 dollars / license for enterprises.

These 3 services also offer a free version, which has a time limit for a meeting, around 40 minutes for Zoom and 60 for Teams and Meet. Zoom monetizes its free version by serving advertisements.

Cisco WebEx

Cisco offers a Meet plan for $15/license and a bundle of meetings+phone starting from $25.

Summary

So, which one seems to be the most cost-efficient for an enterprise?

It seems like the winner is Microsoft Teams, which is cheaper for an existing Microsoft Office customer and it can be a great addition to the Microsoft Office stack, which would offer a seamless collaboration.

Moreover, Microsoft is also a big player in the UCaaS (offering complementary products like Teams Phone – a competitor for Zoom’s Phone system) and will continue to be in my opinion the most dangerous competitor for Zoom.

The UCaaS

The UCaaS space (that includes cloud-based phone) encompasses many strong companies, especially the market leaders like Ringcentral, 8x8, Mitel, Cisco or Microsoft.

A study done by Synergy Research Group shows that RingCentral has around 20% of the market share, while Zoom is just starting to become a big player in the space.

Zoom is only getting started into the UCaaS sector and so far it seems like it was able to leverage its brand in order to generate some momentum. However, future growth will be increasingly difficult for the company as it faces much more and much experienced players in this field.

7. Things to keep an eye for

Here is a summary for things to keep an eye for in order to evaluate how the business is doing:

+ The WFH trend is here to stay. Employees want to be able to partially work from home, putting pressure on the companies to keep the UC services running

+ Phenomenal free cash-flow– the trend must continue into 2023

+ NRR – this metric must remain around 130% in the subsequent periods

+ Remaining performance Obligations (RPO) must continue to grow – even with single digits

+ Rule of 40 – it’s been decreasing – it’s a plus as long as it keeps above … you guessed it, 40!

RED FLAGS

- 11% revenue growth for FY23 which will come entirely from the Enterprise segment (customers attracted by Zooms’ sales team)

In enterprise, we expect that part of our business to grow at approximately 20% year-over-year. Our online business is expected to be flattish for the year – the growth will slow down tremendously.

- Customers’ growth – especially for Enterprise and > $100k segment

- CAC is going through the roof, which also generates a high payback period for the customers attracted. This metric must improve in the next quarters

- Customer penetration remains very small for the newer products – Zoom usually discloses it annually, but watch for it in the earnings reports as well

8. Financial overview

Income Statement

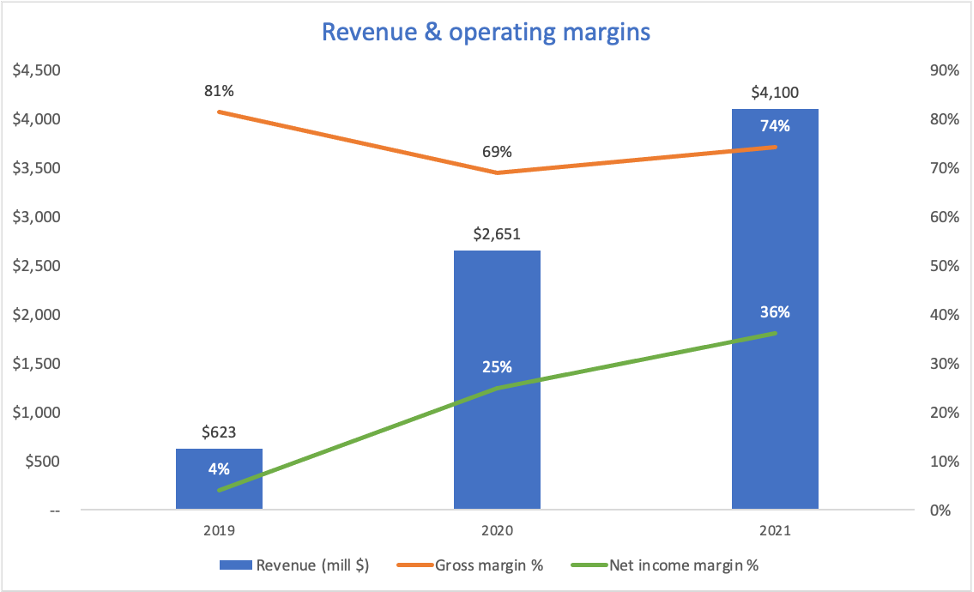

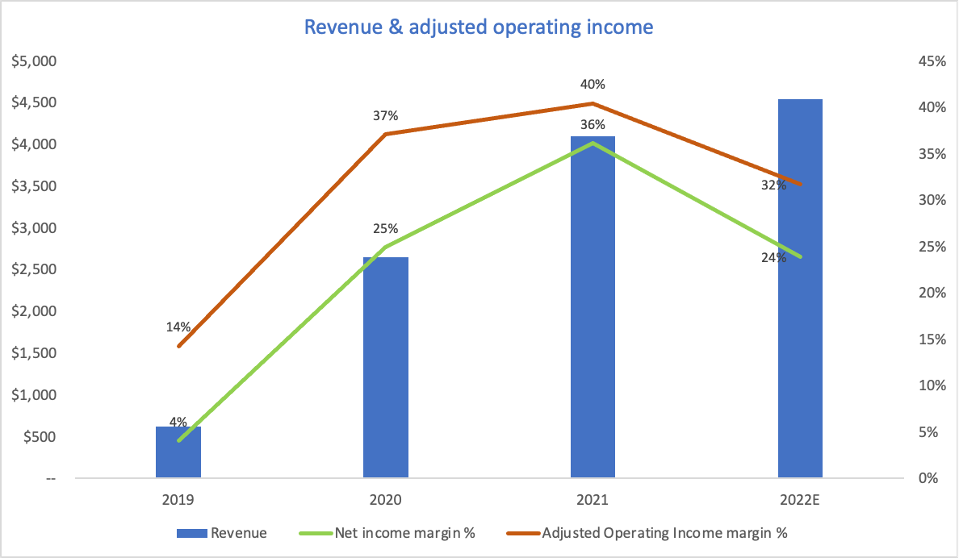

Revenue & operating margins

Revenue grew tremendously for Zoom, as a result of the COVID-19 pandemic. As we can see above, the company has been completely transformed starting with the first quarter of 2020. Although the revenue grew strongly, the gross margin seriously deteriorated and dropped from 81% to only 69% in 2020. Zoom’s CEO was saying in Q12020:

“Our gross margin was impacted by the elevated demand, especially higher levels of free meeting minutes. We have temporarily removed the 40-minute time limit for meetings with more than two endpoints from our free Basic accounts for more than 125,000 K-12 school domains worldwide.

Higher incremental costs also resulted from leveraging the public cloud providers, which was critical to our ability to meet the sudden exponential growth in usage as the crisis spread and governments instituted stay-in-place policies around the world.”

Net Margin

Even if the gross margin decreased while the business grew, Zoom has managed to limit its operating expenses:

Even with the massive growth in Operating expenses, the company grew its top-line much faster and as a result, the operating expenses represented a smaller amount as compared to revenue.

Zoom was already profitable before Covid hit, with a net margin around 4%. The decrease of operating expenses as % of revenue, in conjunction with the pull-forward from the pandemic helped the company improve its net margin, sitting around 36% in 2021.

This is net profit to the shareholders and the metric is indeed extraordinary. It almost begs the question if the company is investing enough in its future growth. I personally would like the net margin to remain around 25% and for Zoom to keep investing the capital in order to generate better returns in the subsequent financial years.

Balance Sheet

In terms of the balance sheet, the things that stand out for Zoom:

- no debt;

- no shareholder dilution;

- huge cash & equivalents position – around 71% of the total assets – the company is continually seeking opportunities for augmenting talent or technology;

- management approved at 31 January 2022 a $1 billion shares repurchase – around 3.3% of the market cap.

While usually a share repurchase is a good sign because it shows that management thinks that the company’s stock will be worth more in the future, in this instance the amount seems really high as compared to the company’s growth opportunities.

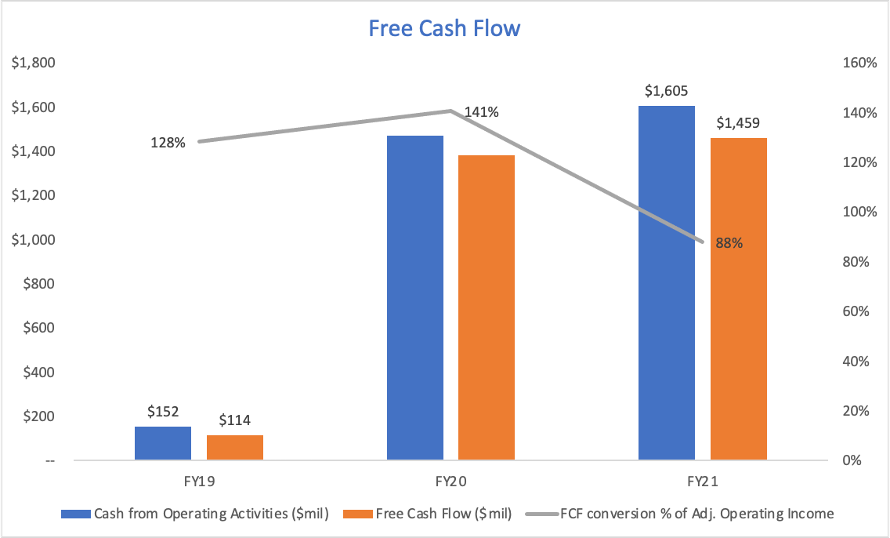

Free cash flow

Free cash flow = Cash from operations – Capital expenditures

Zoom has a tremendous trend regarding the Free cash flow. The company was free cash-flow before 2020, but starting with 2020 it had seen a tremendous improvement. At the end of 2021, the company had almost $1.5 billion dollars in free cash flow for the FY2021.

It represented 88% of the adjusted operation income (operating income including only operating activity), which is a very good sign for any company.

Zoom benefits from a particularly high amount of deferred revenue (unearned revenue) – around $294 million for 2021.

Unearned revenue is the revenue for which the company invoiced their customers and got paid, but didn’t offer their services yet (ex: a contract for 12 months that is paid in the first month). The revenue will be recognized gradually in the 12 months, while the payment can be made at the beginning. The balance for unearned revenue can be found in the balance sheet on the current liabilities section.

The high amount of free cash flow offers Zoom flexibility and multiple options for investing in further growth.

Moreover, this shows that Zoom is generally a light-asset company, that doesn’t require a significant amount of assets to generate revenue. This also applies to most of the software companies that are easily scalable and benefit from low funding requirements.

8.1 Guidance – FY 2023 and beyond

Zoom has guided for a revenue around $4.54 billion for 2022. This represents a modest revenue growth of 11% for the full year.

“We assume that our enterprise business will grow substantially faster than our online business. In enterprise, we expect that part of our business to grow at approximately 20% year-over-year. Our online business is expected to be flattish for the year” – Zoom’s CFO, February 2022

It seems like the organic growth generated by the pandemic will slow down tremendously. This means that Zoom will depend on its sales&marketing efforts in order to keep growing. As we’ve seen before, this was not a great look for the company.

In terms of adjusted operating income (excluding SBC and other non-recurring expenses), it will drop to 32% in 2022 as a result of some investments opportunities that the company will take.

“We are pursuing a massive opportunity, and we will continue to focus on the appropriate balance between growth and margins as we build out and deliver on the potential of our platform.” – Zoom’s CFO, February 2022

9. Valuation and technical

Valuation

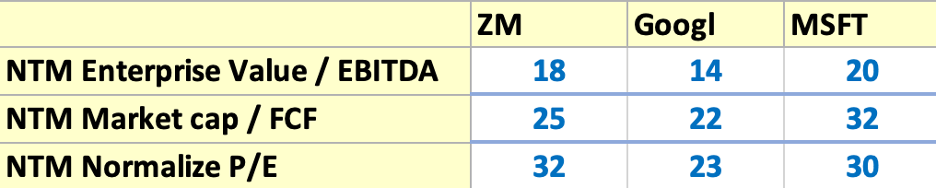

In terms of valuation, Zoom became a lot cheaper during the last couple of months. The company is now in a value-like territory where it became cheap on just about every metric. This comes as a result of the sudden decrease in revenue growth rates. Here’s a summary:

As we can see, Zoom tends to be cheaper than Microsoft and a little more expensive than Google on just about every metric showcased above.

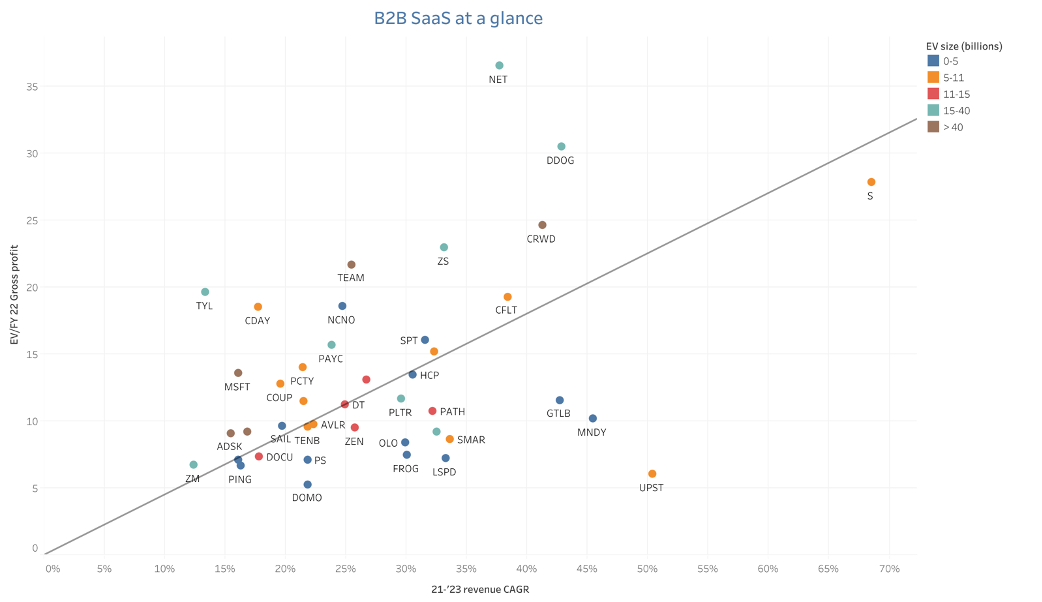

When comparing to other B2B SaaS business, Zoom looks cheap, but we can also see that the company has a compounded annual revenue growth between 2021 and 2023 of only around 12.5%. That’s actually the lowest of all the 40 SaaS companies that I’ve selected and it is also lower than the revenue CAGR for Google or Microsoft.

Technical

Last couple of months have been difficult for the stock market. Between the raising interest rates because of sustained inflation, the war from Ukraine and the oil prices rising quickly, the market has experienced a very high amount of volatility. This leads usually to a decrease of the indices and most of the stocks.

Here’s a photo of the Zoom daily chart:

The stock price action resembles a giant bubble. This might not be particularly because the company is low-quality, but because of the 420% run that it had following the COVID-19 pandemic.

The stock trades now below its pre-pandemic high (the red line around $108). However, since most of the growth is in the past, the company also became much cheaper in terms of valuation multiples. This came as a result of the strong financial performance that Zoom had in 2020 and 2021.

As a conclusion, from a technical perspective, no one knows how low will Zoom go. I have drawn a $62 support that held very well in 2019:

I personally would wait for the price to consolidate for a couple of weeks and of course, I would closely watch the macroeconomic environment since it determines the way most of the stocks go.

As an example, here’s what a period of consolidation may look like (ex from Netflix from 2012):

10. Conclusion

Zoom is a strong business. It has executed perfectly so far, it has a great net margin, a ton of free cash-flow and it launched many new products recently.

However, the company is now trying to make a decisive step from a video-conferencing app to a full unified communications platform. That will inquire a lot of effort, resources and time. Luckily the company has a very strong cash position that it can deploy into acquiring some missing pieces, as well as building some in-house.

The road will be difficult and the competition in intense, since Zoom competes with much bigger, established, deeper-pockets companies. Its execution decides to how much market share can Zoom attract in the new areas where it plans to expand.

To conclude, I think Zoom has plenty of potential and the growth might reaccelerate sometimes in the future, but until I see clear improvements in the factors that I’ve mentioned earlier, I’m not a buyer.

Disclosure: The article only expresses my opinion and it is NOT investment advice. Please do your own due diligence and only pick companies with your desired level of risk