This is the silent killer for Draftkings stock

This is the silent killer for Draftkings stock

Is Draftkings stock a buy?

I’m going to analyze the financials, product, growth opportunities and at the end I’m going to share 7 things to keep an eye for to see if the stock is a BUY.

Cathie Wood certainly likes the stock since ARK is the second biggest shareholder of Draftkings.

1. Company overview

In 2018, New Jersey received a favorable US Supreme Court ruling that allowed the state to legalize online sports betting. Moreover, the decision applies to any other state that wants to legalize online wagering so a new market was born.

Draftkings is a US daily fantasy sports (DFS) and sports betting company. Launched in 2012, with its DFS products and starting with August 2018 it also activates as an online sports betting company.

Draftkings is a market-leader in the online sports betting (OSB) and it is also active in 5 US states with its iGaming offering (online casinos).

Firstly, let’s define some industry specific terms:

Betting handle = bets placed by players

GGR = gross gaming revenue = money players wager – money players win

GGR is the amount for (bets-wins), meaning the revenue for the sportsbook operator.

2.Product overview

Draftkings was launched in 2012 and with its first product, the DFS:

Daily Fantasy Sports (DFS) - offers peer-to-peer play, whereby users compete against each other for prize money.

DFS is available in 44 U.S. states, the District of Columbia, and six international jurisdictions.

Since it was Draftkings’ first product, it represents a big chuck of the business. Although management doesn’t disclose the exact % of total revenues, we know that:

“DFS is in the hundreds of millions of dollars of revenue. It's a very high-margin business, and it is still growing.” – Draftkings’ CEO, March 2022

Starting with 2018, the company was able to increase its product offering:

Online Sports Betting (OSB) - users place bets by wagering money on a sports event

In March 2022, Draftkings was live in 17 US states with its OSB.

This is the second big product for the company and it is believed to be the next “cash cow” after DFS. The OSB is benefiting from strong tailwinds and an increasing total addressable market which helps it grow faster.

iGaming – Also called online casino, offers typically the full suite of games available in land-based casinos, such as blackjack, roulette, baccarat and slot machines.

In March 2022, Draftkings was live in only 5 US states with its iGaming and it is believed that this segment will grow much slower than OSB because of the regulations.

Draftkings Marketplace - a digital collectibles (a non-fungible token, or “NFT”) ecosystem designed for mainstream accessibility that offers curated initial NFT drops (“Primary Sales”).

This is the latest addition to Draftkings’ product suite (launched in August 2021) and it comes as a way to eliminate some of the seasonality generated by the sports schedule.

“More than a third of Marketplace users are new to Draftkings platform. Early cross-selling of new customers to other products was also promising.”

2.1 Business model – How does the company make money?

DFS

Revenue is generated from contest entry fees from users, net of prizes and customer incentives.

Sportsbook and iGaming

Revenue is generated from users’ wagers, net of payouts made on users’ winning wagers and incentives awarded to users.

Draftkings’ revenue is actually the gross gaming revenue, which translates into Bets placed – Winnings.

Draftkings Marketplace

Revenue will be generated as a fixed % take for any transaction made on the platform. However, for now this segment doesn’t have a material impact on the company’s total revenue.

Revenue prospects

The company’s financial prospects depend on legalization of online sports betting and iGaming across more of the United States, a trend that seems to be in its infancy.

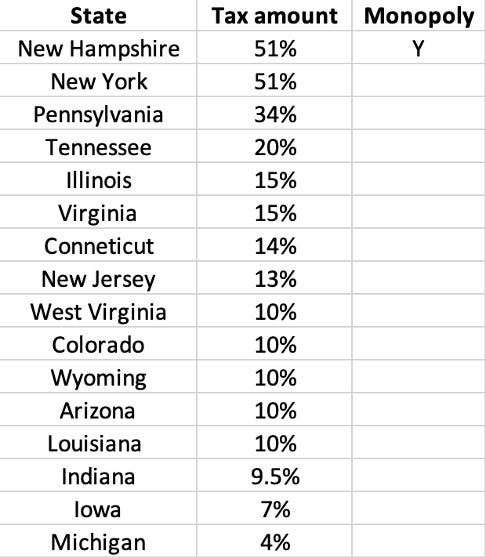

States that have established state-run monopolies may limit opportunities for private sector participants like Draftkings.

On the flip side, there is the potential monopoly offered by a state. Any US state can choose to either encourage a competitive market or chose only 1 operator to receive a license.

For instance, there are 2 US states that offered Draftkings monopoly. Oregon and New Hampshire have agreed it, and in return Draftkings will pay a 51% tax on its gross gaming revenues for New Hampshire.

2.2 Vertically integrated – is it a plus?

Draftkings has been aiming at becoming a virtually integrated gaming operator. In the betting and gambling industry, the games and sportsbetting offering are usually provided by a vendor.

The way in which the operator pays for this service is by a revenue share model. So, for every $1 in GGR, Draftkings would pay a fixed % onto the vendor.

But now Draftkings wants to create everything “in-house” in order to have more flexibility and better margins. It started doing so with its iGaming segment:

And it seems like the results are quick to appear:

So, for the iGaming segment, 60% of the bets were made on in-house game created by Draftkings. That’s a very good trend and I do expect Draftkings to push its games more and gain a bigger slice of the pie.

On the OSB, Draftkings has done exactly the same thing by acquiring sportsbook platform SbTech in 2020 for $3.3 billion.

This deal marked the shift from a 3rd party supplier to Draftkings having its own tech stack. It offers more safety and flexibility for Draftkings, as well as more opportunities for innovation.

3. KPIs

Monthly Unique Payers (“MUPs”)

MUPs is the average number of unique paid users (“unique payers”) that participated in a real-money engagement with one of the B2C products (a DFS contest, sports bet or casino game).

Average Revenue per MUP (“ARPMUP”)

ARPMUP is the average B2C segment revenue per MUP.

Here we have a summary for the two, as well as for the customer acquisition cost:

MUPs grew nicely at the end of 2021, with Draftkings now having almost 2 million monthly paying users.

ARPMUP grew modestly, only 18% YoY at the end of 2021. Usually, the second and the fourth quarter are the strongest for the company, but as we can see below the ARPMUP only grew with 27% and 18% during the last quarters.

Customer Acquisition Cost (CAC)

Besides the average revenue per monthly paying user, we need to keep in mind the customer acquisition cost to see how well the company is investing its sales&marketing budget. Ideally, we would want the customer acquisition cost to decrease as the company adds more customers:

The CAC has grown significantly in 3Q21 (363% YoY) and 4Q21 (44% YoY). Although Drafktings is investing more in Sales&marketing, it is more costly for them to acquire new customers.

However, the company doesn’t disclose a spending per state, which might offer a better image since the company may invest for a couple of months before acquiring any customers in a new-launched state.

Here’s a comparison for CAC and quarterly revenue per paying user:

CAC Payback period

In order to have a better picture, we can see how many years it takes on average for a customer to produce enough gross profit to pay back its CAC.

At the end of 2021, it would take the average customer around 6 years to pay back for its CAC. In the second quarter of 2020 the number of monthly users decreased because most of the sports events closed, so we can’t calculate it for that period.

For full year 2021 the average CAC payback period is around 8 years. That is very elevated because of the significant spending in attracting new customers, in conjunction with a low gross margin (only 39% at the end of 2021).

The company aims to improve its payback period to 2-3 years on a contribution margin basis (non-GAAP metric that excludes external advertising spending).

Revenue retention

The revenue retention rate for Draftkings seems to be good and it’s improving with time.

N stands for customer cohorts considered. It takes into account the length of time spend with the company (ex: 11 customer cohorts are with the company between 8 and 11 quarters, while 2 cohorts are with the company for more than 12 quarters).

In terms of customer retention, the company revealed a 96% customer retention for the states with more than 12 quarters of activity.

Draftkings is improving its customer retention and the revenue per user as the company spends more time in a state.

This is a good trend for the company as it pertains to its existing customers.

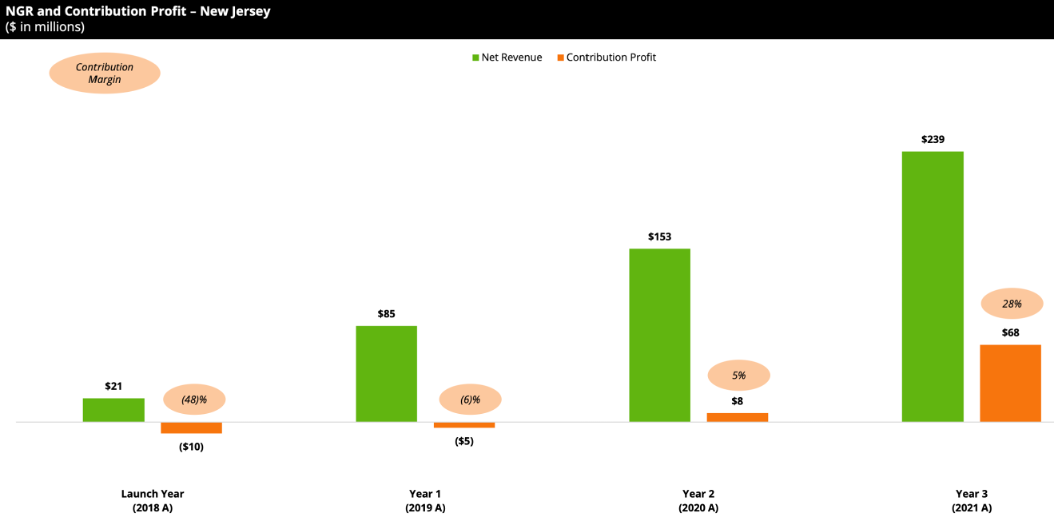

Are any states already profitable?

Another proof of a better execution as the company gains experience is the contribution amount that seems to become positive after 2-3 years. For the first state launched, Draftkings is already contribution positive and the margin grew nicely with around 28% at the end of 2021.

Contribution profit = gross profit – external advertising costs

That doesn’t translate into actual operating profitability, but it does take into account the biggest cost that the company inquires, the external Sales&marketing spending.

“We had 5 states that had positive contribution profit in FY 2021.

We anticipate 5 more states will have contribution profit in FY 2022.” - Draftkings Investor Day March 2022

That’s a good sign for the company. Being contribution positive in more than half of the states where it activates is another thing that demonstrates the improvements in Draftkings’ unit economics.

“If no new states launch for the rest of FY 2022, we expect to be contribution profit positive this year” - Draftkings Investor Day March 2022

This is yet another statement about Draftkings’ strong unit economics. However, the US online market is unique because of its significant growth potential.

As Draftkings is a top 2 player in the market, it will be forced to continue to invest in order to attract new business and stay ahead.

4. Growth opportunities

Giving the nature of Draftkings’ business and industry, the company is forced to adopt a growth-first principle. Here’s how Draftkings describes its growth strategy:

The bigger the market share Draftkings has, the faster it can become profitable. For instance, excluding the 2 states where Draftkings has monopoly, the company becomes profitable faster if it can attain a bigger market share:

“Connecticut only has 2 iGaming operators and 3 sports betting operators. So naturally, we're going to have a larger share in that market and that's the primary reason why it was able to get profitable faster.” - Draftkings’ CEO, March 2022

So, the flywheel for Draftkings could be described as:

Better product -> Higher customer retention -> Biggest market share -> Faster profitability

5. Management team

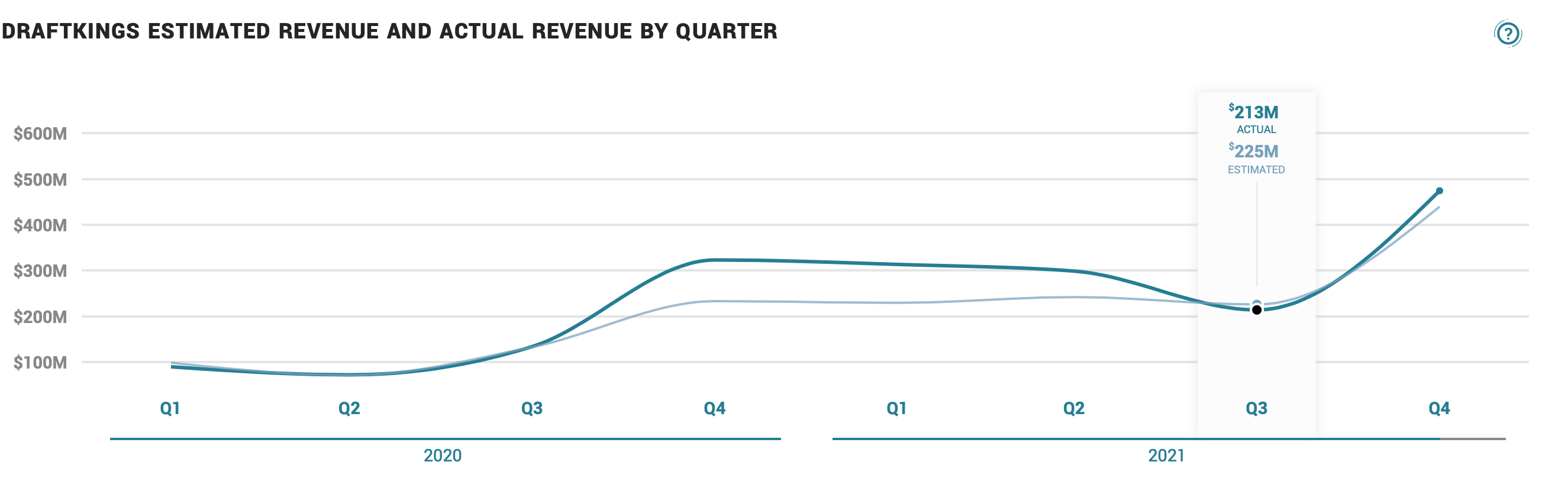

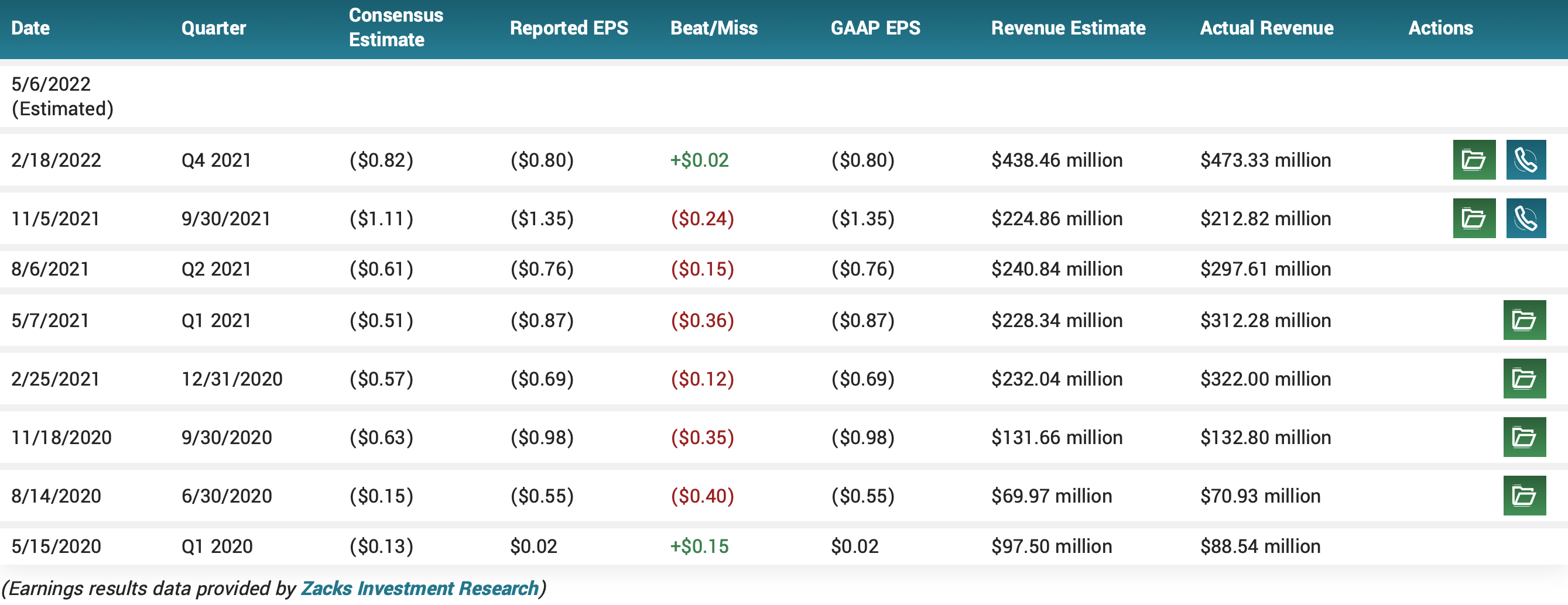

Since it became a public company, Draftkings has delievered on its revenue guidance, except for Q3 of 2021:

Still, on the total 2021 revenue guidance, the company delivered as promised.

However, on the earnings side, since the company has been in hyper-growth mode, it missed earnings estimates on several occasions:

The management owns around 3% of the company, which is a decent percentage for a company the size of Draftkings.

The CEO is also a co-founder, but he only owns around 1.1% of the company. So even if the company is founder-led, the CEO owns a very small %, which is not great for shareholders since the management doesn’t have a lot of “skin in the game”.

ARK Investment, the ETF owned by Cahtie Wood is actually the second biggest shareholder, owning 5.1% of Draftkings, which translates into around $400 million.

6. Industry Fundamentals

Here are 3 crucial elements for the US online betting market.

Barriers to entry

The barriers to entry are high. In order to attract customers, a high amount of sales&marketing spending is necessary.

Still, there are many European established betting companies that will migrate to the US that are willing to invest in order to gain access to this fast-growing new market and they are bringing an experience in attracting new betting customers.

Switching costs

I think there are none. That is a downside for the industry – it is incredibly easy to switch operators, especially considering how many of them are awarding bonuses and rewards in order to attract new customers and their offerings are not really that much different.

Pricing power

It does not apply here. It’s another difficult task to retain customers without having any pricing power, which represents yet another downside for the industry.

Product taxes – a silent killer for Draftkings’ margins

Taxation structure

a) federal tax - 0.25% of total bets

b) state tax – different for every state. For instance, New Jersey applies a 13% tax on gross gaming revenue for online betting.

Here’s a summary for the tax rates that Draftkings pays. The tax percentage applies to the gross gaming revenue (Draftkings’ revenue).

Besides New Hampshire, where Draftkings has monopoly, tax varies between 51% and 4%.

Before 2018, most of Draftkings’ revenue was from DFS, for which Draftkings disclosed a gross margin around 80%. Once the sports betting and iGaming segments grew, these generated much lower gross margin because of 2 variable expenses:

This is Draftkings’ estimate for long-term (year 5) margins. There are two main factors that limit the gross margin for the company:

- payment processing fees – fees charged on user deposits, withdrawals and deposit reversals from payment processors (“chargebacks”) – grew $73 million in 2021 as compared to 2020 and they are expected to have an impact of 8% of revenue long-term.

- taxes – taxes paid grew with $203 million in 2021 as compared to 2020 and they are expected to represent 27% of the revenue.

So that’s already 35% of the revenue that the company must pay to run its business. Let’s say that in time that will decrease to 30%, but considering the remaining elements of COGS (platform and revenue share), the gross margin is still topped around 70%. Not great.

Total addressable market (TAM)

Draftkings was live with OSB in 17 US states (representing 36% of US population) and in 5 US states with iGaming (representing 11% of US population).

Online sports betting has been legalized in 3 more states, representing 7% of the US population, but no operator is live yet. Moreover, 3 states, representing 6% of the US population are legal-pending-launch. So, it is very probable that Draftkings will be launching in at least 3 new US states in 2022.

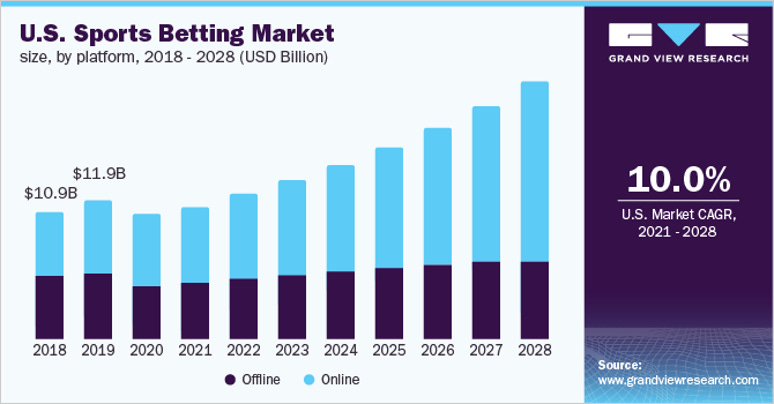

A study published in September 2021 estimates the US sports betting market to grow at a compounded annual growth rate of 10% between 2021 and 2028. Most of the growth will come from the online sports betting:

There seems to be no doubt that the US online sports market will grow. The same trend seems to apply for the iGaming sector, which is also estimated to grow from around $2 billion in 2020 to more than $6 billion by 2025.

To conclude, this is one of the few markets that we know for sure that will grow. And we know because we have a palpable filter for it: the more states legalize online betting, the more the total addressable market grows. So leaving all the estimates aside, we know for sure that every new state that will open will be a good news and a potential market for Draftkings.

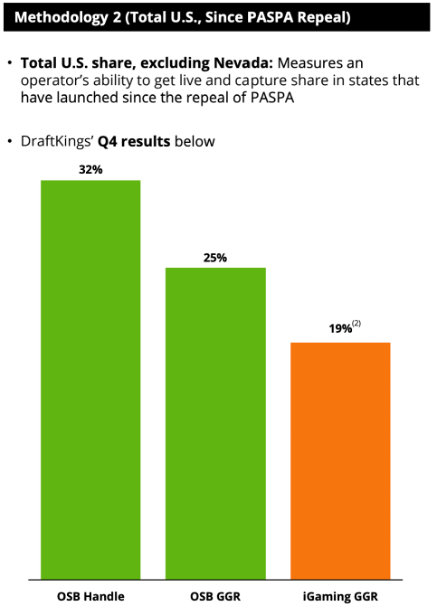

7. Competition

At the end of 2021, Draftkings has 32% of all online sports betting and 25% of all the GGR. On the iGaming side, it has 19% of the total market’s GGR.

Moreover, Draftkings is one of the top 3 US market leaders. The US market seems to be very concentrated around its leaders, as show below:

More precisely, it seems like it’s a 2 players race between Draftkings and FanDuel (owned by European giant Flutter Entertainment) for the player wallet:

Fanduel, just as Draftkings, started with DFS, where it has around 6 million active users.

A study by Bank of America shows New Jersey, Pennsylvania and Michigan as the leaders in terms of online sports betting gross gaming revenue.

In these 3 states FanDuel had a market share around 40%, followed by Draftkings with 30%.

Still, there are many more other competitors like BetMGM, Barstool, or Caesar/William Hill that are also funded by deep-pocketed companies that want to gain some of that market share.

As long as Draftkings will continue to improve its product, I think it has the capability of maintaining its market share and separate itself as a market-leader. Moreover, if the company can sign exclusivity deals with more states, that will only enhance its chances.

8. Risks

Here are the risks involved with investing in Draftkings:

- Hyper-growth company – looks to grow its revenue and invests heavily without a measurable ROI.

- No earnings and no Free-cash flow in sight. The company is burning cash at a fast rate without any real estimates when it might attain profitability.

- Legislative environment might become harsher (possible tax increases along the way)

- The sports betting and gambling are industries that profit off people’s bad habits

9. Things to keep an eye on

+ MUPs to surpass 2 million in 2022 (most probably in Q1)

+ ARPMUP growth – preferably with more than 20%

+ Draftkings’ results in New York in Q1 2022

+ 5 states to become contribution positive in 2022

- High amount of stock-based compensation – I want to see a decrease in the SBC expense

- Gross margin to be improving

- CAC payback period – ideally it will decrease

10. Financial overview

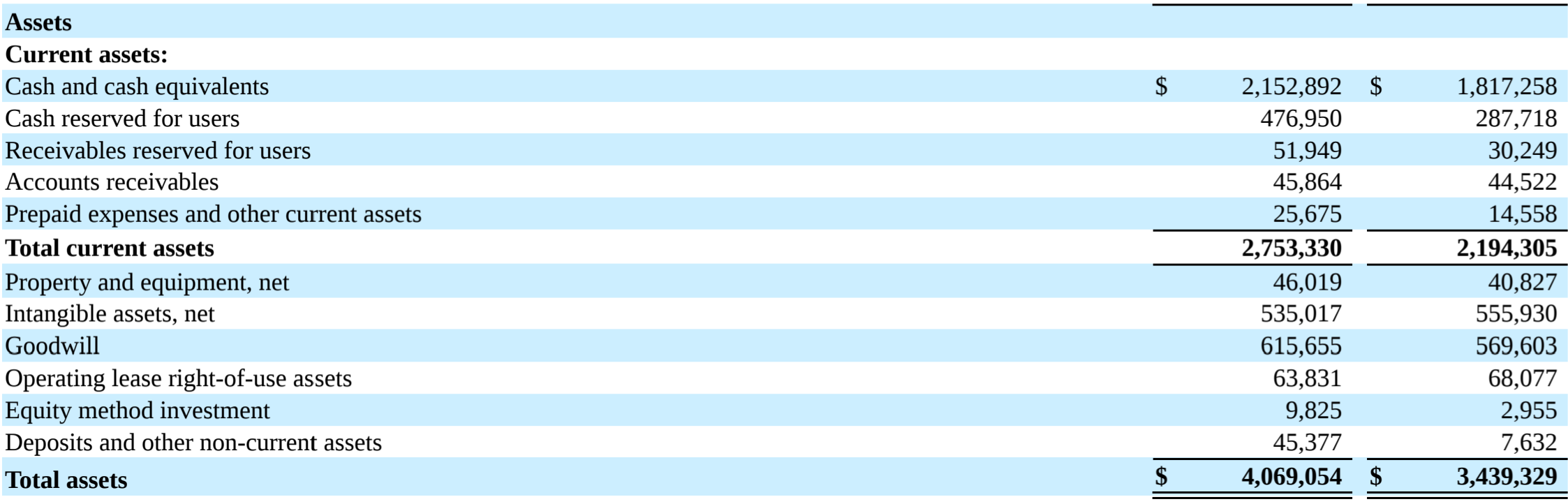

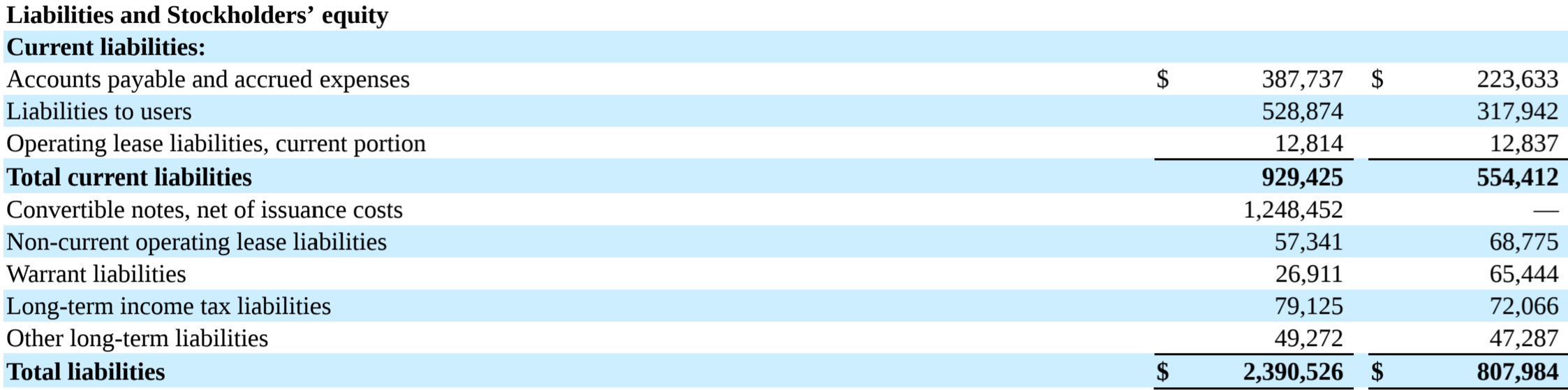

Balance Sheet

Great cash position – 53% of total assets at the end of 2022 - most likely will be used for acquisitions that will improve the company’s product.

On the liabilities side, Draftkings has a $1.2 billion convertible note as debt. It is convertible at a price of $95 dollars, which seems like a far-fetched price, which means that the note will most likely remain as debt.

The main reason why the company issued the debt although it already had a strong cash position is for funding mergers, acquisitions and products investments that DraftKings may identify in the future.

Stock-based compensation

The SBC is a way of maintaining top talent. However, the SBC expense grew 110% YoY as compared to 2020. Moreover, this represents 17% of the company’s total assets. I think this is a high amount and I would like to see it decrease in the subsequent periods.

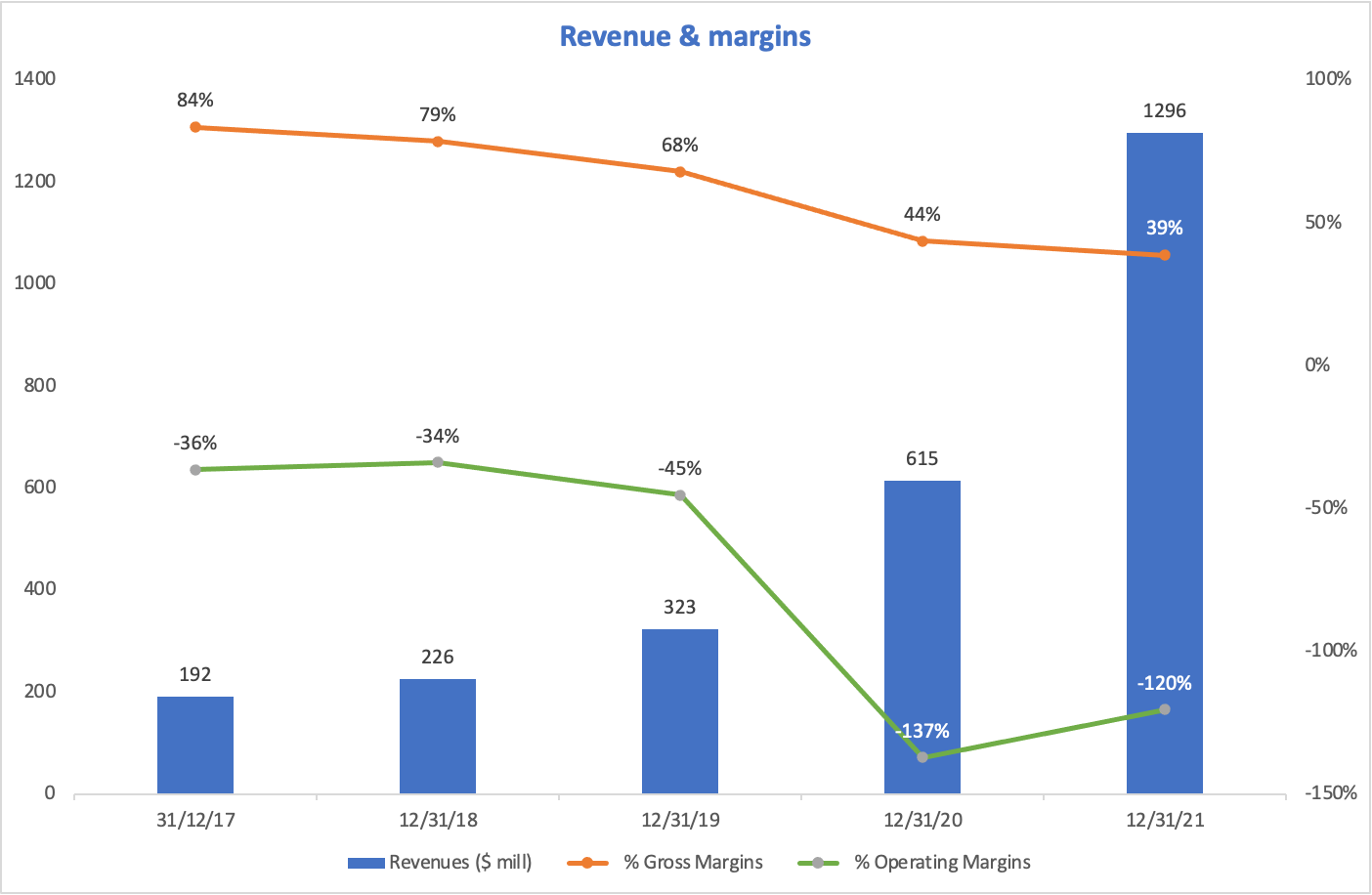

Revenue and margins

Revenue – great trend, 90% YoY growth in 2020 followed by 100% growth in 2021. Phenomenal!

However, the gross margin crumbled. Again, payment processing fees and product taxes were the main cause. As I explained earlier, Draftkings’ gross margin will never be at the levels seen before 2019.

The operating margin has also seen a significant decrease. Here’s a better look at the operating expenses:

2 categories are make for most of the operating expenses:

a) Sales&marketing - activities to acquire and retain players, such as marketing or advertising costs. It is continually growing, but the trend isn’t that bad:

As we can see, in 2021 the S&M budget was lower than in 2020, as percent of the revenue. This is a necessary expense for the company and I do expect Draftkings to have a high % of S&M expenses in the next years as it expands into new US states.

b) General and Administrative expenses

There was a growth of $381 million in 2021, from which around $268 million was associated with stock-based compensation. The rest came mostly from personnel costs reflecting headcount growth.

So why are the margins so bad?

Draftkings could become EBITDA positive within 12 months if no new markets would be launched. However, since the market opportunity is so big and Draftkings is one of the first three operators from the US, the company needs to continue to invest in order to obtain earnings and free-cash flow in the future.

I know what you’re probably wondering:

Not anytime soon. Forecasts predict Draftkings could be EBITDA positive in 2025. That’s still very far away and with one bad quarter, the estimates might be adjusted.

For now, any potential investor in Draftkings must realize that there’s no clear path towards net profitability or free cash-flow. The company needs to invest and will continue to do so in order to attract market share and establish itself as the operator in the sports betting and iGaming markets.

11. Valuation and technical

Valuation

No one knows how to value DKNG. I see these WS analysts going like:

We estimate a $500 million EBITDA in 2026. Now, if we apply a totally random 20X EBITDA multiple and we discount this to today using a 10% cost of capital, we get an $80 price. So that’s our price target.

The only thing that I have against this kind of valuation is that these forecasts can be changed with one bad quarter.

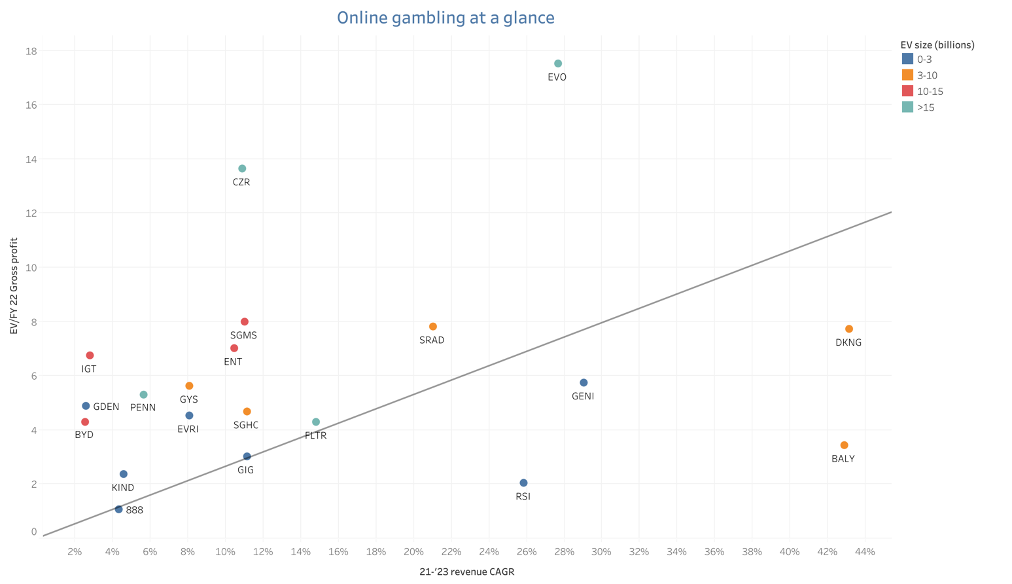

Unfortunately, because of Draftkings’ margins, the company is very difficult to valuate on anything else than revenue or gross profit. However, I’ve compiled a scatterplot with companies from the betting industy, both operators and vendors:

As we can see, Draftkings has one of the biggest compounded annual growth rates in terms of revenue and it is valued around 8X Enterprise value divided by 2022 Gross profit.

Enterprise Value is a more accurate measure of the value of a firm, as it includes the debt, value of preferred shares and minority interest, but minus cash and cash equivalents.

However, recently the market is fond of companies with positive earnings and free cash-flow. Since this doesn’t apply to Draftkings, the company has falled out of investors’ grace recently.

Technical analysis

The trend for Drafkings is definitely bearish. The stock priced declined more than 70% from its all-time high and sits now around $17:

The stock found a short-term resistance around $24 and sits well below the 100 simple-moving average (blue line) as well as the 200 simple-moving average (red line).

I think the stock will consolidate between the $15 to $24 price:

If the $15 support breaks, the stock might hit the $11 price, which was a good support in March 2020.

For now, I would not buy the stock. There’s nothing on the chart that screams bullish to me so I would expect it to consolidate, have a nice rectangle pattern and then have a breakout, especially with good bullish volume.

The next earnings report might trigger this. The company will report earnings for its Q1 2022 in May and we’ll see if the company started the year on the right foot.

12. Conclusion

To conclude, Draftkings has a ton of potential. The company has many tailwinds, which leads to a fast-growing TMA.

I do believe that Draftkings will remain a market leader in the US, but the company is now in a hyper-growth mode, which carries a high-degree of risk.

As we’ve seen recently, the stock market puts a lot of emphasis on earnings and free-cash-flow and Draftkings is just not there yet. It might be over 2 to 3 years, but for now the stock carries a high degree of risk.

Disclosure: The article only expresses my opinion and it is NOT investment advice. Please do your own due diligence and only pick companies with your desired level of risk.