The NFL season is here and I’m betting on this stock

The NFL season is here and I’m betting on this stock

Hi,

I’m back with another in-depth review and this time I’ll describe an interesting sector: online sports betting. In order to do it properly, I need to define two terms that I’m going to be using often:

betting handle = bets placed by players

GGR = gross gaming revenue = the difference between the amount of money players wager and the amount that they win

GGR is basically the amount for (bets-wins), meaning the revenue for the sportsbook operator.

Great, now that I’ve set the field, let’s get into it:

1. Executive summary

Genius’ mission is to become the official data, technology and commercial partner that powers the global ecosystem connecting sports, betting and media. It offers the underlying technology for the collection, integration, and distribution of live data from sports leagues as well as pre-game and in-game odds feeds, risk management services and monitoring of the betting activity for the sportsbook operators. Additionally, it offers personalized online marketing campaigns and fan engagement widgets for betting-related content.

2. Investment thesis

Genius Sports Limited is a fast growing company that activates in an attractive industry. I think in the future it can create meaningful value because of several reasons:

Fast growing TMA fueled by US market liberalization

Following the US market liberalization, sport betting will provide numerous new opportunities for sportsbook operators and their suppliers. The global online sports betting market is predicted to grow at a CAGR of around 13.6% until 2026, providing significant upside for the companies operating within the sector.

Market-leader in data and technology for sports betting

Highly robust technology alongside machine learning and complex analytics capabilities help Genius to capture, process and distribute vast volumes of data points. Genius’ core systems are highly scalable to support ongoing growth in customers, sports event coverage, and volume of bet types. This makes the company one of the two biggest competitors in this space.

High percentage of recurring revenue

Sportsbook contracts are structured with guaranteed minimum payments throughout the life of the term (typically 3-5 years), which allows for good earnings visibility. Over 60% of Genius’ revenue is from recurring revenue generated by the contractual minimum guarantees.

3. Company overview

Why do I like this company? Firstly, it’s a pick and shovel.

It’s not important which operator wins the race for the user wallet, as long as there are operators that need official data for their activity, Genius has a market. The recent outlook indicates that there is a growing demand in the official data market, which makes Genius an important player. Besides being in the middle of the expanding market, the company showcases more particular characteristics that makes it attractive for investors:

a) High switching costs

Genius has constructed a wide portfolio of events, spanned across multiple sports. This kind of portfolio requires a deep understanding of each sport’s technical requirements in order to offer bespoke technology that can support different sports. Genius’ technology is integrated with the sportsbooks’ back office systems and helps the sportsbooks offer their customers odds for the sporting events.

In my opinion, companies that benefit from tight integration into their clients’ businesses have high switching costs, as it is the case here with Genius and the operators. Genius’ software becomes part and parcel of their daily operations, and untangling it from their business to start afresh may be costly, and possibly risky as well since the live betting offering might be affected.

b) Advantages of scale

Another important advantage that Genius’ infrastructure has is its deep integrations within a high number of sport leagues. This creates an advantage because of the scale and can lead to a better and more complex offering from Genius. For instance, its proprietary technology for basketball leagues is now used by more than 180 leagues across 120 countries, which is around 80% of all organized basketball competitions. The Company’s technology framework is standardized, allowing it to support multiple sports leagues at a low incremental cost, which translates into high operating leverage.

c) No customer acquisition cost

Genius and other suppliers of underlying technology needed for online sports betting don’t have to fight for the customer’s wallet. They don’t need to spend money to acquire customers and hence one of the biggest risk associated with the industry, a high customer acquisition cost, is eliminated.

Genius sits in the middle of the industry, between sports leagues and sports betting operators:

The company offers scalable, technology-led products and services to the sports leagues, sports wagering and sports media industries. Genius aggregates the official data for sports leagues and then sells it to sports betting operators. Many of the deals with the sports league are exclusive, which offers Genius an important leg up compared to the competition. On top of official data, Genius provides media and streaming services for operators.

Official data is the feed of live sports statistics that is sanctioned by the sports leagues and federations and it is used to create betting markets, update odds in real-time, and settle bets accurately and timely.

It represents a safe source of data for the sportsbook operators. The use of official data seems to become the norm in the industry, especially the mature sports betting markets, where in-game betting is preponderant. The official odds feed is reportedly a couple of seconds quicker than unofficial versions, which is vital for in-play wagering. Moreover, currently there are two states in the US (Tennessee and Illinois) that require sportsbook operators to use only official league data, as well as some leagues that also require their partners to utilize only official data.

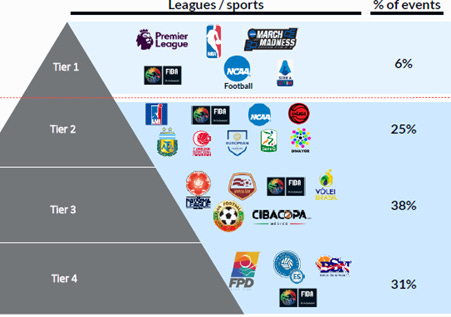

Genius Sports has deals with more than 400 sports leagues, 150 operators and analyzes over 240 thousand events annually. Below we have the events segregation, before the NFL deal:

Genius classifies sports and the associated rights as Tiers 1 through 4. Sports rights classified as Tier 1 are those from leagues with global name recognition, which are typically acquired by rights fees alone. For non-tier 1 leagues (regional leagues with large, dedicated fan bases) Genius acquires the rights via a “contra model”, in which Genius offers technology and software solutions to the sports league in exchange for its official data.

As we can see above, the level of penetration for the Tier 1 leagues is very small. This is definitely an area where the company needs to put in more focus in order to attract more tier 1 leagues, but it may come at a significant cost.

The company estimates that ~94% of their total volume of sporting events offered to sportsbooks come from non-tier 1 sport leagues. This is a huge percentage and Genius is actively trying to acquire more tier 1 leagues exclusive rights. In this sense, it has recently signed a transformative deal for the sought US market:

NFL deal – the leverage in the US market?

In April 2021, Genius and The US National Football League (“NFL”) signed a six year License Agreement, pursuant to which Genius obtains the right to serve as (a) the worldwide exclusive distributor of NFL official data to the global regulated sports betting market; (b) the worldwide exclusive distributor of NFL official data to the global media market; (c) the NFL’s exclusive international distributor of live digital video to the regulated sports betting market and (d) the NFL’s exclusive sports betting and i-gaming advertising partner.

Genius replaced its main competitor, Sportradar, as the exclusive official data partner for NFL. The company will pay $120 million dollars annually, of which half will be paid via stock warrants.

The NFL will receive 22.5 million warrants that grant them the right to buy 22.5 million shares of Genius for an exercise price of $0.01. This makes NFL an investor in Genius, owning around 5.5% of the company (11.5 million shares being currently vested out of the 22.5 million granted).

The way in which the NFL copes with sportsbook operators is via exclusive partnerships that grant the operators the right to advertise on TV around NFL games, access “premium” NFL advertising inventory during games or use the NFL logos across their platforms.

As a result, the operators are committed to buying official NFL data through Genius Sports. So far there are seven operators that are “approved sportsbook operators” for the 2021 NFL season: DraftKings, Caesars, FanDuel, BetMGM, WynnBet, PointsBet and Fox Bet. Only 3 of them have already signed agreements with Genius (DraftKings, WynnBet and Caesars) while the others are expected to do so in the immediate future.

The deal between Genius and NFL is very expensive ($120 million = ~50% of Genius’ 2021 total revenue). However, Genius’ seems to be charging around 4% of operators’ pre-match NFL betting revenues and 6% of in-play revenue, as compared to Sportradar’s 1.5% offering in the past. This puts the company in a favorable position where it can transfer some of the high cost of the deal onto the operators, which will probably reach record numbers this next NFL season.

According to a survey by the American Gaming Association, 45.2 million Americans are expected to bet on the NFL this season, a 36% increase compared to last season's survey. The uptick is attributed primarily to the expanding regulated sports betting market.

What Genius is offering to the sportsbook operators is a full suite of products around NFL (official game data, international streaming, official data for media purposes and Ad Tech space) that will help them acquire customers, engage with them and use options like free-to-play in order to drive their engagement and drive their retention rate.

3.1 Product overview

Genius’ activity is supported by 3 pillars:

1. Sports technology and services offered to the sport leagues – 11% of revenue in FY2020

Genius offers its technology to sports leagues, helping them capture, analyze and distribute their sports data (ex: creation of fan-facing websites, rich statistical content such as team and player standings, immersive social media content and Genius’ streaming product, a tool that allows sports leagues to automatically produce, distribute and commercialize live, audio-visual game content).

The company receives no cash from most of this exchanges and it estimates its value based on the reselling price that it charges the betting operators.

2. Betting technology, Data & streaming – 74% of revenue in FY2020

Genius offers its data-driven technology to sportsbooks: bookmarking, official data, risk management and live audio-video content derived from its streaming partnerships with sports leagues (point 1).

3. Media services – 15% of revenue in FY2020

Through big data analytics of data generated from this unique understanding of fans, live sports events, and the sportsbook market, Genius is able to offer large scale targeted advertising campaigns which are delivered through cost effective, data driven, real time bidding for publishing space.

Genius operates the largest independent media buying trading desk in the gaming industry. It offers data driven marketing products (personalized marketing campaigns for player acquisition) to sportsbooks, leagues and other brands. The company is well positioned to capture a significant part of the sportsbooks marketing spending.

3.2 Business model

Genius usually enters long-term agreements (between 3 and 5 years) with sports leagues for data analysis services and streaming rights that can be sold subsequently to sports betting operators. The contracts between Genius and operators usually contain a fixed minimum guaranteed revenue share amount for the provision of the service.

Genius’ contracts are also structured with a variable profit share arrangement, that allows the company to benefit as its partners grow through increased GGR, expansion to new markets or usage of a more complex data strategy (more events or sports) – meaning Genius takes a slice of the operator’s gaming revenue.

I will shortly describe the 3 sources of revenue for Genius:

1. Sports technology and services – 11% of revenue in FY2020, growing 12% from FY2019

Revenue is generated through the delivery of technology that enables sports leagues and federations to capture, manage and distribute their official sports data, along with other tools and services, including software updates or technical support.

Genius primarily receives noncash consideration in the form of official sports data and streaming rights, along with other rights, in exchange for these services, particularly to non-Tier 1 sports organizations. The company estimates the fair value of the noncash consideration based on the standalone selling price of the services to customers.

2. Betting technology, Data & streaming – 74% of revenue in FY2020, growing 25% from FY 2019

Revenue is primarily generated through the delivery of official sports data for in-game and pre-match betting and outsourced bookmaking services through the Genius’ proprietary sportsbook platform.

Customers can pay either a “fixed” basis, a guaranteed minimum recurring fee for a specified number of events, with incremental per-event fees thereafter, or a “variable” basis, based on a percentage share of the customer’s GGR, typically with minimum payment guarantees.

3. Media – 15% of revenue in FY2020, growing 94% from FY 2019

Revenue is generated from providing data-driven performance marketing technology and services, including personalized online marketing campaigns to sportsbooks, sports leagues and federations, along with other global brands in the sports ecosystem. The services are performed using an input method based on costs to secure advertising space.

Out of the three segments of the business, although the media services part represents only 15% of the total revenue, it grew with an exponentially higher rate in the past year (94% growth in 2020 as compared to 24% in 2019). Management expects media to represent around 20% of Genius’ revenue in 2021 and to progressively grow in 2022 and onwards.

The operators are committing a part of their marketing budgets on the Genius’ platform in order to acquire new customers. They do it by entering long-term agreements, which offers good long-term visibility for the revenues.

Customers categories

Genius has established strong relationships within the industry. With more than 400 leagues as its partners (ex: English Premier League, Germany’s Bundesliga, Italy’s Serie A), it offers its services to more than 300 sportsbooks (ex: Draftkings, Bet365, Fanduel).

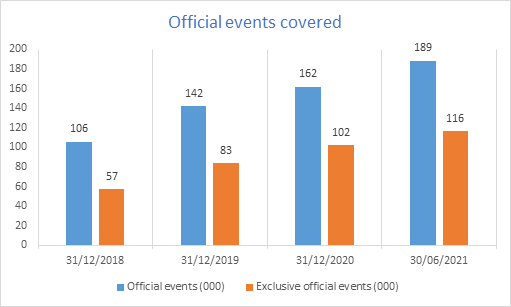

Genius’ rights to collect, distribute and monetize the data related to sporting events may be exclusive (Genius has the exclusive right to collect, distribute, and monetize such data), co-exclusive (Genius shares collection, distribution, and monetization rights with one other company) or non-exclusive. Below we can see the number of events that Genius provides:

Genius hasn’t revealed its customers’ segregation, but no customer has accounted for 10% or more of revenue in the years ended December 31, 2020 and 2019. We don’t have any data about the net retention rate (NRR) of the company, which would be useful for comparing against SportRadar’s 138% net retention rate.

The company expects revenues to become more seasonal than they have traditionally been due principally to the NFL's fixtures running from September through to January.

3.3 Growth opportunities

Although Genius is a fast growing company, the possibilities seem to be massive for its further development. Firstly, the company aims to increase its presence geographically following a market liberalization across the Americas. For instance, in the US the company is now permitted to supply services in 15 US states and will be licensed in all states that will legalize sports betting.

In order to benefit from this liberalization trend, Genius has 2 ways of growing its offerings: covering more sports via new sports leagues deals or adding more services that it can upsell to the existing customers (ex: streaming and other related products or media services for the operators/leagues).

2020 has been a massive year for the company, in spite of the COVID pandemic. The number of events covered was 240k, growing with a staggering 70% compared to 2019.

In terms of its offering, Genius is looking to increase its range of services by investing heavily in its proprietary technology. For instance, the Company expanded into the provision of audio visual (“A/V”) services in the second half of 2019. This includes providing sports leagues with proprietary AI-powered A/V production services to capture live game streams with minimal human intervention.

Acquisitions have been an inorganic way in which Genius chose to expand. The company looks to acquire emerging tech companies to deepen its reach into key sports and it has done it several times recently by acquiring:

- Sportzcast Inc – for around $4.4 million

Sportzcast is a leading U.S. scoreboard data company that developed “Scorebot”, a system that delivers real-time official game data directly from stadium scoreboards. This deepens Genius’ reach with sports leagues and federations;

- Second Spectrum – for around $200 million

Second Spectrum is an official video analytics partner of Premier League, NBA and MLS. The combination will create ‘a complete end-to-end offering’ for the sports, betting and media ecosystem by capturing richer, faster and more accurate data, as well as delivering a fan experience that utilizes augmented video, real-time data insights and predictive analytics;

- Spirable – amount undisclosed

The company allows brands, agencies and rights holders to create, automate and optimize highly personalized content. The company’s platform is complementary to Genius’ existing media and advertising products, expanding the company’s ability to deliver fans contextually relevant and personalized content;

- FanHub – amount undisclosed

A leading Free-To-Play game provider – the company adds new F2P game offering to increase fan engagement and customer retention and to offer a more personalized user experience for sports fans.

4. Management team

Genius is led by its CEO and co-founder, Mark Locke. The company was launched in 2001 and it specialized in aggregating sports betting data before switching to providing outsourced odds making solutions to sportsbooks. In 2015 Genius Sports Group was born as a software provider of sports and media technology. This extensive growth period gives us an idea about the experience of the company’s CEO. The Chief Commercial Officer and the Chief Technology Officer have both been with the company before 2015, more precisely since 2012 and 2009 respectively.

The management team owns a significant part of the company, with the CEO holding around 11.2% of the outstanding shares assuming full exercise of the underwriters’ options.

Another aspect that I personally like to focus on is the quarterly earnings reports and how these compare with the company’s estimates. Unfortunately, Genius became public in December 2020 and they’ve only reported earnings three time.

However, in the latest ER, the management revised its revenue guidance for FY2021 to $255 - $260 million after initially raising it from $190 million to around $250 in the previous ER, putting the company on track to surpass its initial guidance for FY2022. The management team has also adjusted the guidance for EBITDA, which will now be ~ $16 million, lower than the initial estimate of $25 million because of costs associated with getting listed as a public company and some other investments.

The management has been devoting the last two quarters towards execution of their core strategy (growing via strategic acquisitions while finalizing breakthrough deals with sports leagues and operators) and it seems like Genius is setting up nicely for future expansion.

5. Industry Overview

Sports betting market

Although the global online betting market is expected to grow at a rapid pace, I will focus this analysis on the sports betting part of it, which represents around 40% of the total market, making it the most popular activity for online gambling:

In 2021, sports betting revenue (GGR) is forecasted to reach $2.5 billion and, by 2025, this figure is anticipated to grow to $8 billion, growing at a CAGR of ~34%.

Betting and fantasy are predicted to become key industry drivers in the next 3-5 years, with an anticipated yearly growth of 7.2%. These favorable forecasts are mainly due to the rapid acceleration of the betting market in the United States since the lifting of the federal ban in 2018 - PwC’s Sports Survey 2020

The US market – the sought for market

In the US market it all started in 2018. Although the state of New Jersey tried to legalize sports betting since 2011, it has been a bumpy road. More precisely, between 2011 and 2018 the state of New Jersey had several attempts at making online betting legal, but without much of a progress.

In 2018, New Jersey received a favorable US Supreme Court ruling that allowed the state to have sports betting. Moreover, the decision applies to any other state that wants to legalize wagering.

Shortly after, more states starting legalizing online sports betting and as of now, 15 US states allow online sports betting with many more states allowing only some type of betting (ex: in-person) and more states currently filing legislation aimed at legalization.

Europe:

The global online sports betting market is predicted to be around $59.5 billion in 2026, growing at a CAGR of 13.6%. Europe led the online sports betting industry in 2019 with a volume of $12.14 billion, and it is projected to hit $26.32 billion by 2026 growing at a CAGR of 12.1%. With a market share of 48.6% in 2019, Europe is the largest contributor to Mobile Online Sports Betting.

In Europe there are several countries, such as Germany, that remain in the early stages of liberalization and proliferation of sports betting. H2 Gambling Capital expects Europe to generate an estimated $20 billion in GGR in 2025, increased from an estimated $12 billion in 2020. Europe remains a key market for Genius due to its large scale and relevance within the global sports betting industry.

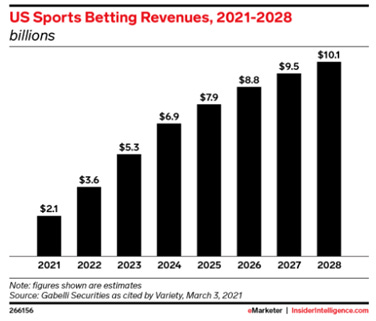

Many sources are weighting in on the potential for this sector. Other companies estimate the US sports betting revenue (GGR) in the same ballpark, with around $10 billion in GGR by 2028:

5.1 Existing trends

Technology developments

While the sports gambling industry grew explosively, mobile and online technologies are used to create seemingly unlimited types of wagering opportunities.

For instance, around 23 million Americans were planning to bet on the 2021 Super Bowl. Amongst them, a record of 7.6 million were willing to bet with online sportsbooks, up 63% year-over-year.

Online gambling is available any time, providing more convenience and privacy. According to World Advertising Research Center (WARC), around 73% of internet users (nearly 3.7 billion people) will access the web solely via their smartphones by 2025, instead of more traditional methods such as laptops or desktops. The launch of 5G will also enable people to use their phones because of faster download speed, better connectivity and an overall better experience.

Moreover, in mature markets such as the United Kingdom, in-game betting currently represents the majority of total bets by Gross Gaming Revenue (“GGR”), making it a critical offering for all major sportsbooks. For instance, Genius’ CEO estimated during Q2 ’21 ER that for some European operators (ex: Bet365) the percentage of wages made during the game can be as high as 79%.

This seems to become the trend within the US market as well:

We've heard from one major U.S. sportsbook that 40% to 50% of all wagering is now in-game. The industry is nervously trending towards the use of official data as its most secure method of powering regulated sportsbooks, protecting customers and helping to fund its sports - Mark Locke, Q2 2021 Earnings Results

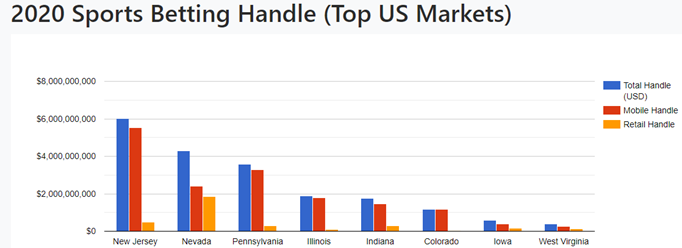

As we can observe above, in terms of betting handle (bets placed by players), New Jersey set the standard for the US sports betting in 2020, creating the most prolific mobile sports betting market in the nation. This might of come as a consequence of the COVID-19 pandemic, that forced Atlantic City (New Jersey’s betting capital) casinos to close from mid-March through the end of June, with the casinos only allowed to operate at 25 percent capacity through the end of the year.

6. Competition

Although there are a handful of companies that offer similar services to Genius’ (ex: Stats Perform, IMG Arena), their biggest competitor is Sportradar. With a bigger presence in the world of sports betting, Sportradar is the more established company, that has already attained net profitability in the more mature markets where it operates (Net profit around $15 million for FY2020).

Sportradar just became a public traded company at a price around $27, which values the company at around $8 billion.

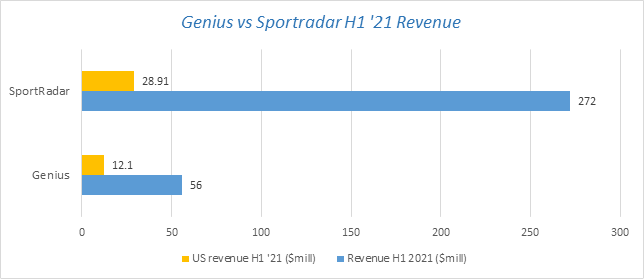

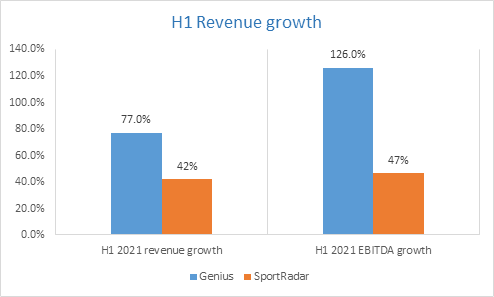

Both companies are currently targeting the US market as an organic way of growing and as of now, Sportradar generates more US revenue. However, Genius is the fastest growing enterprise and has attained a leg up by swooping the NFL deal from Sportradar in Q1 ’21. Below we can see a short comparison between the two companies in terms of revenue (both of them have around 11% of the total revenue coming from the US):

I must highlight that in my opinion, the online sports betting environment can host many providers of live fee data. However, some sports leagues will offer exclusive rights for the aggregation and distribution of their data. In this case, other competitors can still offer a non-official set of data to their customers, but it will be of inferior quality (it can have a latency of a couple of seconds, as there is the case with the NFL data that SportRadar will continue to supply to its customers that are not partners of the NFL).

The current environment can set up the stage for a duopoly in the sports betting industry with both competitors creating value for their investors.

7. Risks

Despite the COVID-19 pandemic, both Genius and Sportradar had positive revenue growth compared to 2019. However, the growth has been recorded during the second half of the year, when most of the sport leagues restarted. However, 2020 was a special year and the sports betting results have been fueled by the lockdowns. In this sense:

a) the significant growth that the market experienced in 2020 might have been partially fueled by the sudden closure of the physical casinos. For instance, world-renowned places like Los Angeles or Atlantic City have been substantially impacted by the COVID-19 pandemic with the latter one only functioning at a 25% capacity from June to December 2020.

b) once people spend more money outside of their homes, they might decrease their wallet amount, which would lead to a recency bias which might be skewing the estimates for the future growth of the sports betting market

More risks involve the hefty premium that Genius paid for the NFL deal, which might not materialize into created value, difficulties in integrating the new acquired companies, unsuccessful business model or significant struggles encountered when trying to expand the media segment for non-betting customers:

Gambling in general is a sensitive topic for brands and advertisers. Regardless of legality, it's just not typically a place that some of the more conservative brands want to be. That’s not to say there won't be participation or that gambling won’t attract more advertisers, but at least with the biggest brands, there are question marks - JoAnna Foyle, senior vice president of inventory partnerships at The Trade Desk

8. Financial overview

From a financial perspective, things are looking good for Genius. With no long-term debt on their balance sheet, in conjunction with a strong cash position following their public listing and second offering done in June 2021, the company seems to have a green light towards executing.

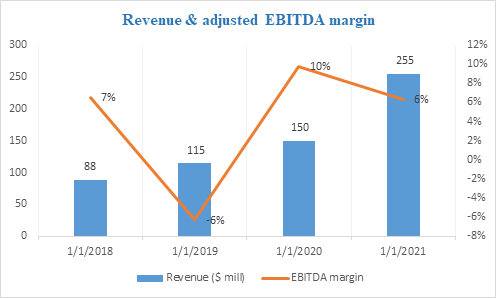

The Income Statement portrays the company as a high grower, with revenue growing at 31% for both 2019 and 2020. In spite of the temporary closure of sports during the COVID-19 pandemic, Genius managed to grow revenue and achieve the highest ever margin for adjusted EBITDA. The 2021 numbers are official estimates from the company:

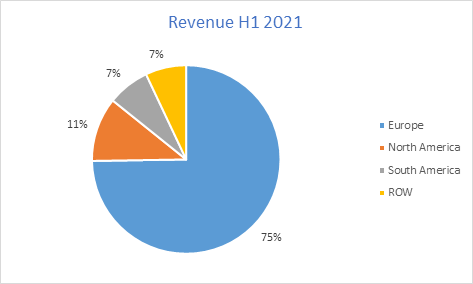

From a geographical aspect, Genius has recorded around 75% of its revenue from Europe. It is not surprising giving the fact that Europe is the more mature market, as detailed before. The US is catching steam and represents around 11% of Genius’ total revenue in the first 6 months of 2021:

The company raised its FY2022 revenue guidance during the last earnings report, estimating a range between $255 and $260 million for 2021, growing at 70% compared to 2020. Additionally, because of the one-time costs associated with becoming a public company, Genius estimates its adjusted EBITDA margin for 2021 to be around 6% while its long-term target is around 40%.

An important factor in achieving its long-term target for EBITDA is the gross margin. It hasn’t been great during the last couple of years as it pertains to a SaaS business or some of the sports betting operators (ex: DKNG has consistently had over 50% gross margin). The company had a good gross margin in 2018, around 40%, but since then it wasn’t able to replicate that:

Cash flow

The cash flow statement looks well for a high growth company. The operating cash flow is positive, which means the company’s operations generate cash, which is a good indicator for the business.

However, when considering the capital expenditures, the free cash flow will become negative primarily because of the purchase of intangible assets. Still, the company doesn’t need to be free cash flow for now as long as it stays in the hyper growth mode.

Stock based compensation

NFL warrants

In relation to the NFL deal, the company has granted the NFL a total of 18.5 million warrants (for the first 4 years of the deal) that make NFL an investor. The warrants have an exercise price of $0.01 and 11.25 million of them are already vested. The fair value at the grant date is around $15.63. This is the value used for recognizing the cost related to the issuing of the warrants. So far, around $198 million dollars have been expensed and around $91 million remain unrecognized stock-based compensation expense related to the warrants.

Additionally, and unrelated to the NFL deal, the company closed their legacy management incentive plan, which was in place prior to the SPAC merger. This has resulted in another non-recurring non-cash equity charge in Q2 of 2021 of a one-off stock-based compensation charge of approximately another $200 million.

Both of these transactions are equity, non-cash transactions that the company included in the Q2 of 2021 results, as It follows:

Of course, for a clear picture of the company’s activity, adjusted EBITDA nullifies the impact that these one-time expenses have on the income statement.

Although it is a great way of keeping the management focused on future growth, stock based compensation will cause stock dilution for the existing investors, which has a negative impact as it reduces individual investment value. I will follow closely the next quarters to make sure this meaningful expense remains a one-time only occurrence.

9. Valuation and technical

Below we can see the evolution of the NTM (next twelve months) Enterprise Value / Revenue. As we can observe, the multiple decreased really fast, from a high of 27.7 to a current value of around 11.9. This was after the market sell-off in the spring of 2021, which cut the valuation multiples for most of the growth stocks:

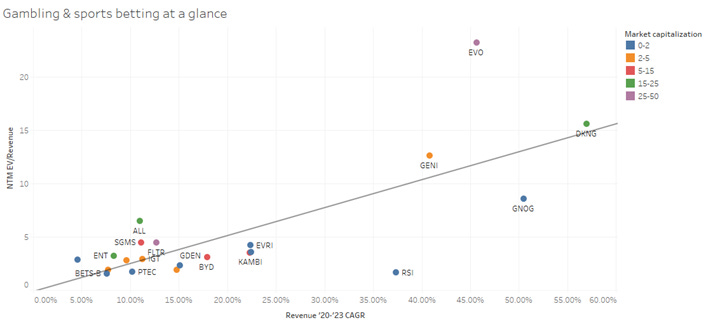

In order to compare Genius to some of its peers, I have compiled a scatterplot with some companies from both the gambling (casino) and sports betting industry. I’ve also included some sports betting operators like Draftkings or Flutter Entertainment and I’ve compared their revenue CAGR (compounded annual growth rate) for the period 2020 to 2023 to their NTM EV/Revenue.

It is easy to see that Genius sports sits above the trend line, which means that when considering these two metrics, the company trades at a premium (R2 = 0.56; p-value < 0.0001):

As far as the current trend of the stock, the company has been in a nice, healthy uptrend recently. The stock sits near the anchored VWAP (purple line) and the 100 SMA (blue line) on the daily chart:

We can see two major areas with high activity: a support around $14.5 and a strong resistance around $22.5. After the recent uptrend, the stock has found some resistance around $23 and a double-top like pattern seems to be forming. I do not predict the stock will crumble, but I do expect it to pull back a little more, perhaps to the 200 SMA (red line) or the recent trendline (green line trending upwards), especially after the strong 50% rally in the last two months.

Since the company became public via a SPAC, another important aspect is related to its public warrants. The company announced during the last ER that it plans to redeem the warrants soon, which can see in the price of the warrants, that hold almost no time value. So a good way of investing in the company is by stocks or LEAPS:

We are also cognizant of the fact that we may, over the course of the next few months, have the option to redeem our outstanding public warrants - Nicholas Taylor, Genius Sports CFO, Q2 2021 ER

10. Conclusion

There are a ton of ways in which Genius Sports can grow. After entering the US market, the company must navigate carefully through the multiple opportunities and pick the best use for its capital. Finalizing multiple commercial deals, as well as acquiring intensely will fuel a period of remarkable growth as well as many challenges. Still, I trust that the management is well suited to run the company and provide the best value for its investors.