The future of real estate

1. Introduction

1.1 The industry

Real estate industry is huge and highly fragmented. In the US alone there are sold annually approximately 5 million houses with a total value of around $1.6 trillion. As of November 2020, less than 1% of the transactions are made online.

Furthermore, around 89% of the buyers and sellers are using a real estate agent. This process translates into high commissions and moving costs. Moreover, the duration of the whole process can be lengthy in most cases.

Opendoor Technologies looks to disrupt the real estate market by fundamentally improving this process.

1.2 The company

Opendoor Technologies operates the leading iBuying digital platform in the US, enabling consumers to buy and sell homes instantly. By offering an integrated digital experience, it provides the sellers with a cash offer in an all-digital procedure. The same goes for buyers, who can self-tour homes and get in-app financing without the need to ever meet an agent.

Opendoor utilizes its proprietary platform based on data science in order to deliver competitive home valuations. A seller can receive a cash offer in as fast as 3 days since no repairing is done until the house is sold. The repair costs will be retained from the selling price and are done solely by Opendoor.

However, if the seller feels like the offer from Opendoor doesn’t consider the house’s unique characteristics, he/she can actually negotiate with the platform in order to obtain a higher price.

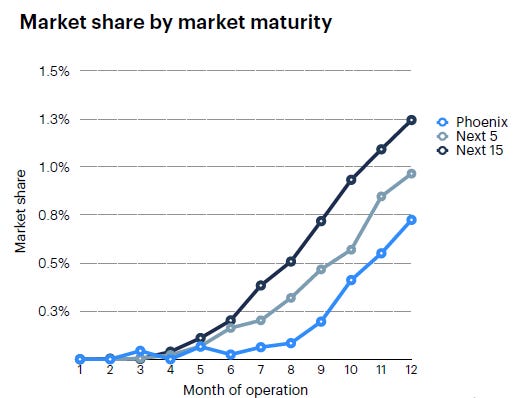

The company operates in 21 markets in the US, having only 2% of the market in these areas. For its first 6 markets, the market share is about 3.2%:

Due to their infrastructure, Opendoor thinks it can now gain market share much faster than in the past. Once the blueprint is set, it may have an easier job of captivating market share, as proved by their most recent markets. This may be one of the reasons why the company has set a very optimistic objective for 2021: to double their market footprint in 2021 from 21 cities to 42.

1.3 Management team

Founded in 2014, the company is currently led by the founder and CEO. It is an encouraging sign for a fast growing company to have of the original management team still running the show. Additionally, the insider percentage is around 9%, which is a relatively high percentage for a newly listed company.

2. Covid-19 pandemic

Although Opendoor is continuously improving its operational process, the company has been tremendously affected by the COVID-19 pandemic.

Opendoor stopped acquiring houses in March and has actively managed its portfolio by selling the vast majority of its inventory in Q2 and Q3. Starting with Q3, the company has been aggressively acquiring houses, reacting to the strong market demand that characterized the second half of 2020, ending the year with 1827 homes in inventory (triple from September 2020).

The total homes sold in 2020 was 9913, declining 47% from 2019, while revenues came in 45% lower than in the previous year. Moreover, Opendoor has been forced to reduce its staff by 35% in an effort to lower operational costs and maintain decent operational margins.

3. Risks

While the real estate market presents some unique risks, most notable are:

- the increase in interest rates might be a headwind for the recent trend of the real estate market;

- a strong HPA (home price appreciation) might also diminish the appeal for buying a property - around 10% price gain at the end of 2020 ;

- business model may not sustainable long-term – being a capital intensive model, it is based on high volume and low margins;

- ferocious competition;

4. Competitors

Besides the local real estate agents, Opendoor also competes with innovative brokerage companies like EXp World Holdings, but its main competitors are Zillow and Redfin.

Both these companies have a wide range of real estate services, iBuying being the last addition for them. Redfin has created its RedfinNow service, while Zillow operates Zillow Offers, both offering a service for online buying and selling houses.

Revenue for Zillow Offers came in at $1.7 billion (has grown 25% in 2020, from $1.36 billion – represents 51% of Zillow’s revenue), while Redfin Now generated $210 million (decreasing 13% from $240 mill in 2019 – represents 24% of Redfin’s revenue).

There are 2 conclusions from these metrics: Zillow has around 50% of its revenue from iBuying, while Redfin has only 24% and judging by the revenue it is obvious that Zillow is the biggest threat for Opendoor in the iBuying segment.

Secondly, Zillow has managed to grow revenue in 2020 compared with 2019. So it adapted better to the pandemic, mostly because of the higher inventory that it possessed.

5. Financials

For the last quarter of 2020, Opendoor has managed to surpass revenue estimates ($249 million vs $244 million), but it missed significantly the earnings estimates (loss per share of $0.23 vs $0.12).

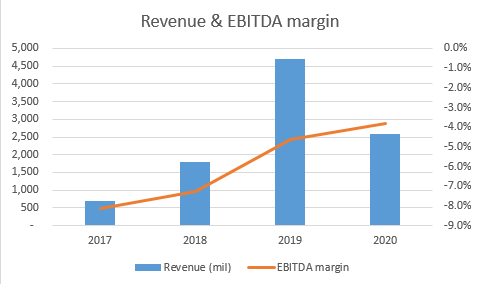

Before the COVID-19 pandemic hit, Opendoor was the undisputed leader in the iBuying segment. With 18 800 houses sold in 2019 and approximately $4.7 billion in sales, it proved the interest from the public towards the iBuying model. Below we have a summary of how the company looks from a financial perspective:

At a glance, we can see that EBITDA margin has improved over the years, which is definitely a good sign. Moreover, the company has managed to cut losses short during the pandemic and has adjusted in order to have its smallest EBTIDA loss percentage to date. However, since the company is still in the growth phase it didn’t manage to become EBITDA positive yet and the management estimates this will happen in 2023.

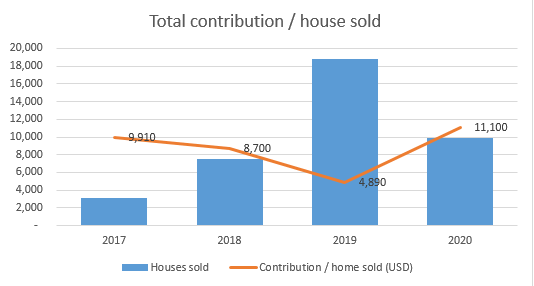

Another important margin for Opendoor’s unique business model is the net contribution per house sold:

Total contribution is defined by Opendoor in its S-1 filing as:

Total contribution = Total revenue - Net Purchase Price - Net Repairs - Holding Costs - Selling Costs

The net dollar contribution has peaked during 2020, improving significantly compared with 2019. This is an encouraging trend, as the company aims for $18K / home as a long-term target for the contribution margin.

5.1 Future outlook

For now, the company offers adjacent services like title & escrow (title makes sure the seller has the right to sell the house while escrow supervises the exchange of funds) or home loans / refinancing.

Even so, the company looks to launch many more complementary services like home warranty, home insurance, upgrade &remodel or moving services. These look to change the focus from just selling a house to orchestrating the entire moving process, while generating a significant increase in CM.

In this regard, Opendoor finished 2020 with a lot of cash on its balance sheet and it is heading into 2021 with good momentum. Having raised a substantial amount of cash after becoming public via a SPAC, followed by a second offering in Q1 2021, it sits on approximately $2.3 billion that it plans on using it for aggressive market expansion and other ventures that will accelerate business and product development.

6. Valuation and technical

Here I will compare the two biggest competitors in the iBuying sector: Opendoor and Zillow:

As we can see from above, Zillow is growing its presence in the iBuying segment by investing heavily, as proved by a notable negative EBITDA margin. This confirms that Zillow is making serious efforts to benefit from the growing online trend.

It is evident that right now investors percept Zillow as being more attractive (a higher P/S), as well as an almost double EV/Revenue. The difference in valuation applies for future P/S as well, as Opendoor trades at only 1.77 Price/Sales for 2021.

However, given the fact that Opendoor is the faster growing company and the market leader for iBuying and with analysts’ estimates for 2021 CAGR at 80% (source: Yahoo Finance) as well as targeting a massive market expansion, Opendoor might close the gap in valuations (EV/Revenue might increase, getting closer to Zillow’s), offering upside potential to the investors.

Taking into account all of the above, I think Opendoor offers a good risk:reward ratio and we can see below 2 technical areas where an entry would be suitable: the 20 recent short term support and the 15 area that has acted as a long term support.

Conclusion

To sum up, it is obvious that before the pandemic hit, the customers were attracted to the convenience and speed of transacting with an iBuyer. With a massive market still untapped, Opendoor is positioned well for massive market expansion and numerous growing opportunities.

The trend of digital transformation will definitely take time and will surely have its obstacles (as the recent COVID-19 pandemic), but I believe that Opendoor will have the strength to surpass these difficulties and create a true one-stop shop for homes.

As a potential investor, I think we can see massive upside potential and Opendoor might be a terrific long-term investment for 2021 and years to come.

Disclosure: I am long Opendoor. The article only expresses my opinion and it is NOT investment advice. Please do your own due diligence and pick companies that have your desired level of risk