Roku summary research report

Roku summary research report

Hi,

I’m back with another in-depth stock review and today I’ll be describing one of the most beloved stocks during the COVID-19 pandemic. Roku’s stock is now 50% lower than its all-time high and this might be a great moment to invest in the business:

1.Executive summary

Roku is one of the streaming pioneers and one of the biggest players in advertising industry. In this report I will focus on the fundamentals of the business and I’m going to shape an image of the company. Starting with its mission:

Our mission is to be the TV streaming platform that connects the entire TV ecosystem around the world. We connect users to the streaming content they love, and we enable content publishers to build and monetize large audiences and provide advertisers with unique capabilities to engage consumers

It is pretty clear what the company’s mission is: to help people navigate from linear TV to streaming while enjoying a wholesome experience.

Usually, the companies that are trying to create a major shift in paradigm present the biggest risk, but they can also offer the biggest return for their shareholders.

2. Investment thesis

- Global CTV leader in terms of streaming time

- Tremendous edge in targeting and optimizing advertising campaigns, given by its first-party data from more than 50 million users

- CTV is the fastest growing video advertising platform as cord-cutting intensifies around the world

3. Company overview

Roku is a software and ad-tech company founded in 2002 in the US. The company started by selling hardware digital media players that could be connected to smart TVs. In 2014 the company launched its own branded connected TVs that were equipped with its proprietary software.

The company has benefited from significant tailwinds generated by the COVID-19 pandemic and has grown its top line with over 50% during the last four years. Roku did a phenomenal job so far in terms of competing with much bigger players for the connected TV space.

As of now, the company is valued at around $30 billion and in this analysis, I will highlight some of its fundamentals to see if Roku might be an attractive investment.

3.1 Product overview

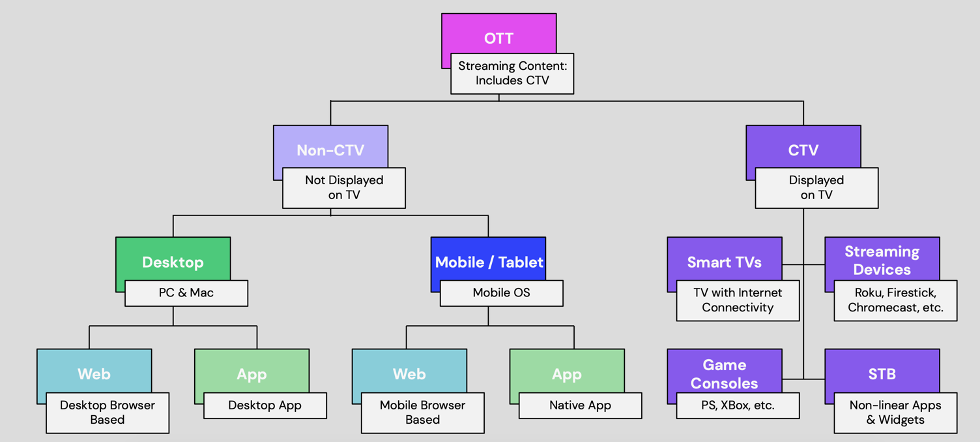

CTV (or “connected TV”) refers to the viewing of digital content on internet connected televisions, including through stand-alone streaming devices, gaming consoles and smart TV operating systems. CTV has some meaningful benefits like superior targeting, measurable results and a growing audience.

There are three main types of internet video streaming, VOD (video on demand) models:

SVOD = Subscription Video on Demand – Netflix, HBO, Disney+

A service that allows users to access an entire library of videos for a small recurring fee.

TVOD = Transactional Video on Demand – PPV events

A service that allows you to buy content on a pay-per-view basis (the user is charged per video or video package rather than gaining access to the entire catalog).

AVOD = Ad-based Video-on-demand – Youtube, The Roku Channel

A service that is usually free to its consumers and ad revenue is used to offset production and hosting costs.

Roku’s product suite

Roku platform

“Central to our platform is the Roku operating system (the “Roku OS”). The Roku OS is purposely built for TV and designed to run on low-cost hardware which allows us to manufacture and sell streaming players that are affordable.” - Scott Rosenberg, Roku Senior Vice President

Roku Streaming Devices

Roku streaming devices run the Roku operating system (Roku OS) purpose built and designed specifically for TV. The Roku OS powers Roku players, Roku® Streaming Sticks™ and Roku Smart Soundbars.

Roku TV

Roku TVs, manufactured by OEM brands around the world (TCL, Hisense, Philips, JVC etc) use Roku’s purpose-built OS and TV hardware reference design. Co-branded Roku TV models are available through direct sales at major retailers (Walmart, Target, Amazon, BestBuy).

Distribution

In the United States, the majority of Roku’s streaming players, audio products and Roku TV models are sold through traditional brick and mortar retailers, such as Best Buy, Target and Walmart, including their online sales platforms, and online retailers such as Amazon, and to a lesser extent Roku’s website.

Amazon, Best Buy and Walmart collectively accounted for 69% and 72% of the player segment revenue for the years ended December 31, 2020, and 2019, respectively.

Engagement

The company believes that offering users a wide range of content drives increased user engagement by delivering a better overall streaming experience.

From the Roku home screen, the users can easily find and access more than 500,000 free and paid movies and TV episodes including live TV, news, sports, hit movies, popular shows, and more that are available from the thousands of channels on the streaming platform.

3.2 Key investment areas

Ad-based Video-on-demand (AVOD)

AVOD channels are appealing to consumers who are facing subscription fatigue among the proliferation of subscription video on demand (SVOD) services like Netflix and Disney+.

The proportion of consumers using an AVOD service has increased from 34% in February 2020 to 58% in February 2021, according to Hub Research.

A study done by the Horowitz Research in June 2021, found that 48% of the US TV viewers use AVOD as a way of watching free content. Second is FAST, a way of watching free live linear TV, with 29%.

From the 48%, The Roku Channel is one of the main platforms that support AVOD streaming, only behind Google’s YouTube.

")

Moreover, in other geographical areas, such as Latin America, more than 87.8% of adult internet users said they watched subscription video content, while 70% of streaming users reported viewing content on free AVOD platforms.

A study from Criteo found 61% of Americans say subscription cost is their top consideration for using a video streaming service. The survey found 3 in 5 are happy to watch video streaming services with a fully or partially ad-funded subscription. Trade Desk found 64% of consumers don’t want to spend over $30 each month on streaming video, making ad supported content more appealing.

The Roku Channel is set to roughly half the ad load - half of a full ad load that you would have on traditional TV.

However, the Achilles heel of AVOD is the fact that if you're that AVOD service, you actually do not know who's watching your content. Unless there’s a log-in, you don’t’ know who's watching. You don't have an account; you just click on the app and you can look around and watch stuff.

As a result, when publishers are trying to monetize that content, they're monetizing it very similar to traditional TV. And so, the CPMs are very low there. Unless you're the platform owner, right?

“As the platform owner, we know who's watching because you're signed into your Roku account to be on the platform. We can get better recommendation for content because we have a sense of who you are, what you may like based on some other behaviors you had. And then when we go to monetize that same content that might be on a stand-alone AVOD service that's getting monetized at a low CPM, we can serve a targeted CPM there. So, it allows us to monetize it as a much higher CPM rate than they could. And that is a big advantage around The Roku Channel.” - Steve Louden, Roku’s CFO, January 2021

Insert The Roku Channel (TRC)

The Roku Channel is Roku’s own streaming channel that drives user engagement on the platform by providing users with free, ad-supported access to a large library of third-party content that Roku directly licenses, in addition to content made available through The Roku Channel by our content publishers (creators like HBO can provide Roku some of its non-premium content to be streamed on TRC under the AVOD model), as a source for advertising inventory.

Through Premium Subscriptions within The Roku Channel, Roku resells ad-free premium content subscription services from providers such as Showtime, Starz, and Epix directly to their users. TRC can also be accessed on competing devices (ex: FireTV, Samsung OS).

“We use our knowledge of our viewers and the data we have to find out what's going to perform well on The Roku Channel. We also use that data to target promotions, the appropriate content promotion based on the user.” - Steve Louden, Roku’s CFO, May 2021

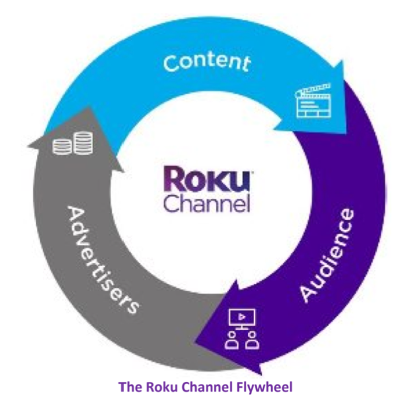

The network effect – Roku’s moat?

A moat is best described as a business' ability to maintain its competitive advantages in order to protect its and market share and long-term profits from competitors.

The Roku Channel flywheel is the perfect way for TRC to grow: it attracts users by creating better free content using the revenue from advertising.

That’s how the network effect moat is best showcased: the more people are using the platform, the better the platform will become.

Regarding the number of users, TRC had around 70 million accounts in Q1 of 2021. Since then, management didn’t report the evolution of their activity, but they cited:

“The Roku Channel is growing extremely fast. And this is a big driver of our P&L. It's growing much faster than the overall platform and even the AVOD, the ad-supported segment overall” - Scott Rosenberg, Roku Senior Vice President

As a way of offering great AVOD content, Roku launched a content studio that will create short-form TV programs, interactive video ads and other content for The Roku Channel, its AVOD offering.

Recently, besides licensing ad-free premium content subscription services from its partners, Roku has decided to enter the market of content creating.

In a very risky and potentially costly move, Roku announced that it will develop more than 50 shows over next two years. New York Post reports that the budget will be “on par with basic cable shows”, which translates to a $250,000 to $750,000 investment per unscripted episode and $500,000 to $5 million per scripted episode.

International expansion

“International is one of our key investment areas. We've outlined in the past that we have 4 key investment areas: international expansion, Roku TV, The Roku Channel and advertising.

Our international strategy involves the same 3 phases business model that we adopted in the U.S., which is focus first on growing active accounts, then on increasing engagement and then on monetization. And so internationally, we're still primarily in the growing active account phase” - Anthony Wood, Roku’s CEO in Q4 2020 ER

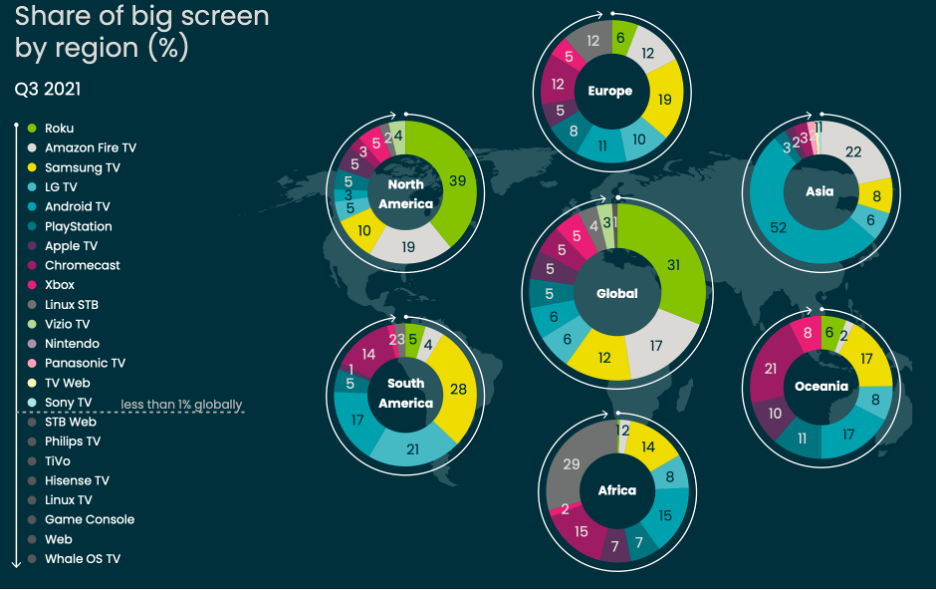

As we can see below, Roku is global leader in term of streaming time, with around 30% of the viewing time in Q3 2021. It is followed by Amazon’s Fire TV and Samsung’s Tizen OS.

The biggest source of screen time for Roku is North America, where Roku has around 37% of the viewing time, followed by Amazon with 22%. However, we can note that Roku is basically non-existent in areas like South America, Africa or Asia.

“In 2020, 38% of smart TVs in the U.S. that's sold were running the Roku operating system. So, we have surpassed Samsung. We're also the #1 TV OS in Canada with 31% of the smart TV market.” – Steve Louden, Roku’s CFO, January 2021

A study conducted by the Hypothesis Group in October 2021 showed that Roku is the #1 TV Streaming Platform in Mexico, based on hours streamed. In addition, the study found that consumers in Mexico view Roku as the best streaming platform for free TV shows and movies.

One of the most prolific markets for streaming Europe, where countries like Germany had almost 50% of the households connected to a SVOD subscription at the end of March 2021, with Amazon Prime and Netflix leading the way.

However, Roku’s presence in Europe is insignificant. As a result, Roku launched its streaming devices in Germany in September 2021, but the company definitely lost the start to Amazon Prime, who sells its Fire TV sticks since 2015 and to Google who sells its Chromecast devices since 2014.

In the UK, Roku launched its Roku TVs in June 2021 in an effort to catch up with the other players from the streaming platforms market.

3.3 Business model – How does the company make money?

Revenue

Player revenue is generated primarily from the sale of streaming players. We expect to continue to manage the average selling prices of our streaming players to increase our active accounts. As a result, player revenues may not increase as they have historically. We expect that the tradeoff from player gross profit to grow active accounts will result in increased platform monetization and gross profit.

Platform revenue is generated from the sale of digital advertising and related services, content distribution services, subscription and transaction revenue shares, Premium Subscriptions, billing services, sale of branded channel buttons on remote controls and licensing arrangements with service operators and TV brands.

Content publishers (the streaming services hosted on Roku’s platform) also have access to Roku’s promotional and audience development tools to help them attract and retain viewers.

Content publishers can use a variety of ad placements, including native display ads on the Roku home screen or a screen saver to drive channel downloads, promote a channel’s content, and direct traffic to their channels in order to drive subscriptions or movie and TV show consumption. Of course, all of these are additional sources of revenue for Roku.

Seasonality

Roku has historically seen seasonality in the business related to advertising and streaming player sales. Roku’s revenue and gross profit are traditionally strongest in the fourth quarter of each fiscal year and represent a high percentage of the total net revenue for such fiscal year due to higher consumer purchases and increased advertising during holiday seasons.

Furthermore, a significant percentage of our player sales through retailers in the fourth quarter of the fiscal year are pursuant to committed sales agreements with retailers for which we recognize significant discounts in the average selling prices in the third quarter in an effort to grow our active accounts, which will reduce our player gross margin.

KPIs

I am going to describe now some of the operating key performance indicators that are used to evaluate the company’s activity and what its revenue is dependent on:

The company defines active accounts as the number of distinct user accounts that have streamed content on the platform within the last 30 days of the period. Users who streamed content from The Roku Channel only on non-Roku platforms are not included in this metric.

2021 has seen much slower growth in active accounts for Roku, reaching numbers below the analysts’ expectations. This might showcases that:

- Roku needs to expand internationally as fast as possible because the US market might be saturated;

- TV prices have been significantly higher in 2021 because of the supply chain disruptions, which led to inflation and represented a headwind for the company’s ability to attract new users;

Hours streamed

Roku earns platform revenue from various forms of user engagement, including advertising, revenue shares from subscriptions and transactional video on-demand.

However, Roku’s revenue from content publishers (ex:Netflix, AppleTV) is not tied to the hours streamed on their streaming channels, and the number of streaming hours does not correlate to revenue earned from such content publishers.

In essence Roku only monetizes more streaming hours for its AVOD content. For the SVOD/TVOD it earns revenue with each new subscription acquired with Roku Pay.

Average Revenue per User (ARPU)

The company defines ARPU as the platform revenue for the trailing four quarters divided by the average of the number of active accounts at the end of the current period and the end of the corresponding period in the prior year.

ARPU measures the rate at which Roku is monetizing its active account base and the progress of its platform business. As we can see above, the company did a great job in increasing its year-over-year ARPU, growing it consistently with more than 45% over the last two quarters.

However, some parts of the business are growing much faster than the rest. For instance, TRC has been growing much faster than the AVOD segment:

“The Roku Channel is growing extremely fast. And this is a big driver of our P&L. It's growing much faster than the overall platform and even the AVOD, the ad-supported segment overall” - Steve Louden, Roku’s CFO, May 2021

3.4 Roku’s ability to monetize

Rate of TV streaming and advertising shift to OTT (over-the-top) is a decisive factor for Roku’s performance:

Ability to monetize users and streaming hours

Roku’s platform makes it easy for content publishers to distribute and monetize their streaming content through three primary business models: TVOD, SVOD and AVOD.

The company generates revenue from TVOD and SVOD channels from various forms of revenue sharing arrangements. Their revenue sharing arrangements generally apply to new subscriptions for accounts that sign up for new services and to movie rentals or purchases for TVOD.

Roku Pay – for SVOD or TVOD content

Roku Pay, the platform’s billing solution, is a key platform capability that simplifies consumer subscription signups and drives purchase and retention for partners.

Roku Pay gives publishers a robust payment platform for increasing conversions and maximizing subscription revenue. The price paid by the publishers for using Roku Pay is a flat 20% platform fee:

Revenue from the distribution of AVOD channels is generated through the sale of advertising within the channel, via a RAF model:

Roku Advertising Framework (RAF) – for AVOD content:

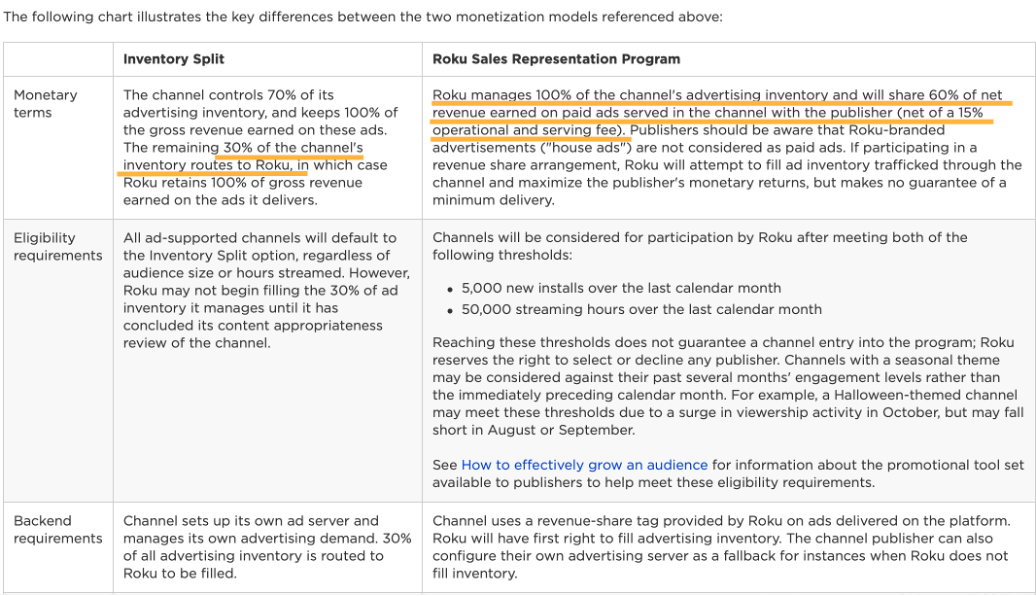

There are 2 ways in which Roku monetizes its AVOD segment:

Once a publisher (streaming service) becomes eligible for the Roku Sales Representation Program, the company will charge:

15% as operational and serving fees

40% of 85% => 34%

Total fees charged by Roku = 49% of gross revenue earned on paid ads

Customer concentration risk

As of September 2021, no customer accounts for more than 10% of Roku’s net revenue. For the platform segment no customer accounts for more than 10% of the revenue, while the player business is split between three of the biggest retailers: Amazon, Best Buy and Walmart.

3.5 Roku’s Advertising platform

Roku’s Ad Manager

Roku Ad Manager allows advertisers to target to the right streamers through exclusive Roku audience data, while allowing you the flexibility to control campaign budgets, audiences and goals.

Roku Ad manager is a self-serve ad-buying tool that will allow content creators and advertisers to manage channel promotional campaigns within the Roku ecosystem:

A self-serve ad-buying tool means that Roku will sell the software to an ad agency and the agency’s traders will use the software to buy advertisement space. The agency is fully in control of the campaigns and Roku will only charge a platform fee for the software that it provides.

Roku’s OneView

OneView (originally DataXu) is a Demand side platform (DSP) that has been acquired by Roku in 4Q19 for around $150 million. It allows marketers to plan, buy and optimize their video ad campaigns that run on Roku’s devices and services.

Roku data, measurement and inventory are natively available for buyers within the OneView Ad Platformenabling buyers to transact programmatically, buying inventory from both Roku and publishers directly, all while leveraging Roku’s proprietary first-party data, measurement and optimization capabilities.

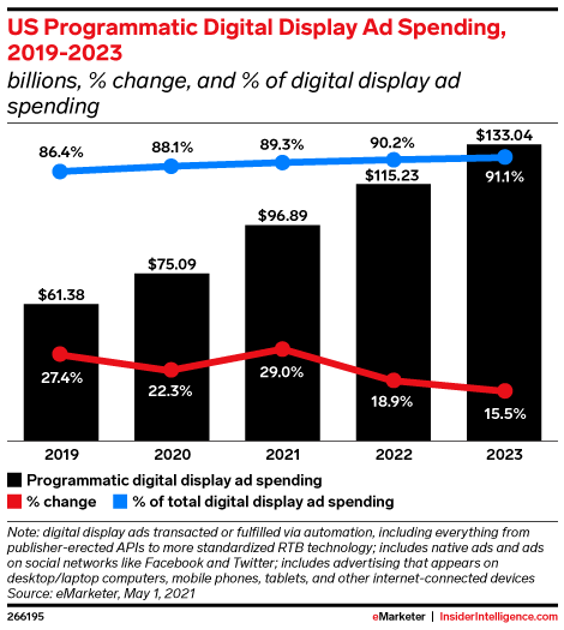

OneView’s platform has some characteristics that make it attractive for the advertisers: programmatic advertising is automated, incurs a low cost and it can be very effective in targeting specific audiences or demographics. Programmatic advertising became a reliable way of buying advertising for most agencies and has showcased significant growth recently:

On the publisher side, Roku owns all the ad space supply for The Roku Channel and it takes an additional cut from the publishing partners, depending on the size of the publisher.

“In Q1 2021 total TV streaming ad impressions delivered through OneView nearly tripled year-over-year, while total impressions on the Roku platform (sold by Roku or its publishers) more than tripled.” - Steve Louden, Roku’s CFO, January 2021

OneView can also activate as an independent DSP and it can buy ads for both Roku’s inventory, as well as for other publishers from the “open internet” (all publishers excluding Google, Facebook and Amazon) because of its really strong cross-screen use cases. For instance, using its ACR (automatic content recognition) software to retarget a user on desktop and mobile based on what content or advertising they're interested in or conversely using site visitation information to inform what ads are run on the large screen. As a result, OneView remains a premium product.

The programmatic advertising space is well known for its high chunk of fees paid to intermediaries (around 37% in 2020 according to eMarketer), only around 60% of the revenue budgets actually go to the publisher. Since Roku has its own demand-side platform, it can sell its publishing space directly to advertisers, hence retaining a much bigger percentage of the advertising budgets, in conjunction with a higher CPM for CTV as compared to linear TV.

With over 14,000 streaming services on their OS, Roku offers flexible pricings for advertisers, like CPM (Cost per thousand impressions) or CPI (cost per installation – pay when a user installs).

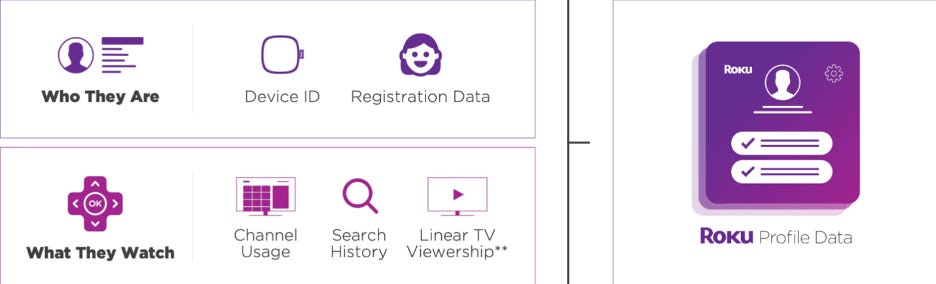

Roku’s first-party data

Using its video automatic content recognition (ACR) software, Roku can track what its users are watching, if they have given their opt-in consent to receive marketing materials based on their activity. For example, while on Facebook.com the user might receive targeted ads based on what he reads, writes or likes in the newsfeed.

Roku has first-party data (data collected directly from the audience) from more than 50 million active users in the US.

3.6 Growth opportunities

Acquisitions

In terms of acquisitions, Roku has been involved recently in two types of transactions:

a) Acquisitions of TV shows and libraries of content:

In March 2021 Roku acquired a content company, TOH (“This Old House”), America’s No. 1 TV Home Improvement Program for around $98 million.

Acquisition of TOH includes 1,500+ Episode Library, Production Studio, Two Ongoing Series of Top-Rated Original Programming, and Related Digital Assets to Support The Roku Channel’s Growing AVOD Service. The company may continue to acquire new content for its TRC platform and rebrand it as "Roku Originals".

b) Acquisitions of technology

In March 2021 Roku acquired the Advanced Video Advertising (AVA) business from the information, data and market measurement company Nielsen for $47 million.

The deal includes Nielsen’s video automatic content recognition (ACR) and dynamic ad insertion (DAI) technologies in an effort to accelerate the launch of an end-to-end DAI solution for traditional TV that can now bring to the ad inventory the same kinds of targeting, measurement and optimization that is available for streaming services.

Roku actually had embedded these solutions into their televisions for the last 5 years. So now the company owns the tech and the intellectual property around it as well as the ability to do linear ad replacement on the fly.

4. Management team

Roku is led by its CEO and founder, Anthony Wood. He founded the company in 2002 and has been the CEO since. He is also the chairman of the company since February 2008. In terms of reviews, Anthony Wood has a good score on Glassdoor.

Regarding the ownership, the CEO owns around 17.2% of Roku. This is a very high percentage and shows high influence from the management, especially voting power.

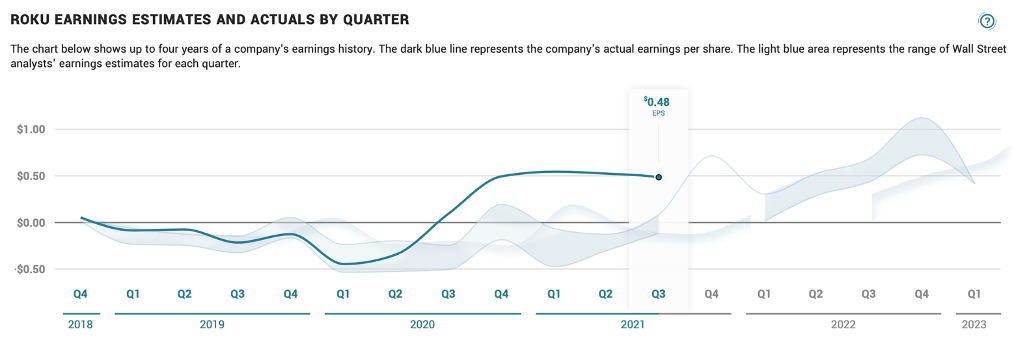

In terms of revenue and earnings guidance, Roku has a great track record. The company has consistently exceeded analysts’ expectations for both revenues, as well as earnings:

Management seems to be a great plus for the company and sets high expectations for the company.

5. Industry Overview

TAM

Roku’s total addressable market is the $60 billion dollars that advertisers spent in 2020 in linear TV advertising. The amount keeps growing and some of that amount seems to be following consumers into the streaming space:

")

Since all of its inventory comes from CTV, Roku is a pure play method to invest into the growing CTV industry. Roku offers access to the young demographic and to the people that already chose cord-cutting.

“If you look at TV time in the U.S. today, adults 18 to 49 spend 42% of their TV time streaming. But if you look at the amount of ad spend on streaming versus traditional TV, only 22% has moved to streaming.

There's this big gap still and that gap is starting to close, but has a long way to go. The rate of that closure because they will catch up eventually, and the rate of all viewers moving to streaming, those are the biggest drivers of our ad business, which is a $60 billion opportunity.” – Anthony Wood, Roku’s CEO in Q3 2021 ER

The advertising upfront process

A yearly event where media companies, advertisers and publishers negotiate in advance the advertising inventory for the next twelve months and set the terms of the deals (CPM = cost-per-thousands of impressions).

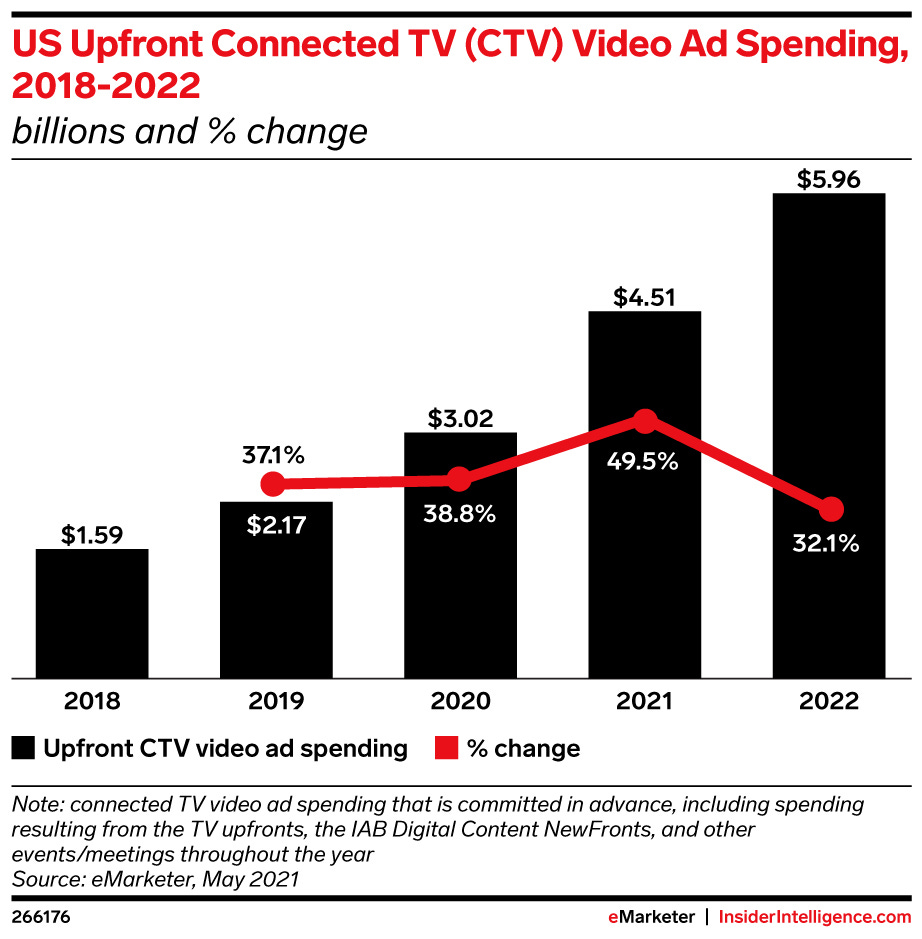

eMarketer estimates that the upfront for CTV has grown with ~50% in 2021 as compared to 2020, with around $4.5 billion being committed in 2021. Moreover, 2022 will also provide an estimated 32% growth in the CTV upfront.

On July 12 Roku announced they had finished their upfront negotiations and said that year-over-year they had doubled their upfront spend commitments. Moreover, 42% of 2021 business is coming from first-time advertisers.

5.1 Existing trends

Why is the CTV advertising space attractive?

eMarketer forecasted that advertisers will spend around $14.44 billion on CTV ads in 2021, a 60% growth compared with 2020:

Ad Spending, 2019-2024 (billions, % change, and % of total media ad spending)")

This is just a fraction of the total $81.58 billion spent on digital display ad in 2021.

The adoption of CTV has disrupted the traditional linear TV distribution model, as eMarketer estimates that approximately 31.2 million U.S. households have "cut-the-cord" (i.e., canceled a pay TV service and continued without it) as of the end of 2020, and this number is expected to increase to close to 50% of all U.S. households by the end of 2024. This disruption has created new options for consumers and new economic opportunities for content sellers to compete with traditional linear TV.

Was the pandemic the peak for streaming content?

The “Evolution of Entertainment” report from NPD highlights that the time spent watching TV shows and movies in the United States in the first half of 2021 rose 4% over last year, as screen-entertainment spending declined by 1%.

Even if people spent more time outside, the number of movie releases in cinemas remained below than the pre-pandemic level, the bigger macro trend that we see unfolding is the migration from linear TV into streaming.

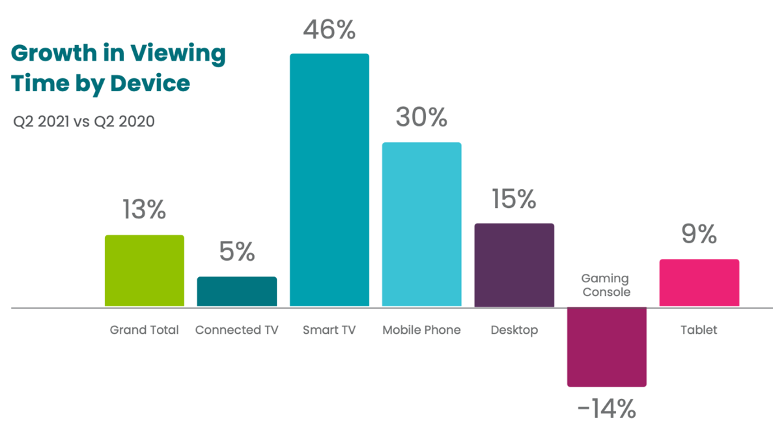

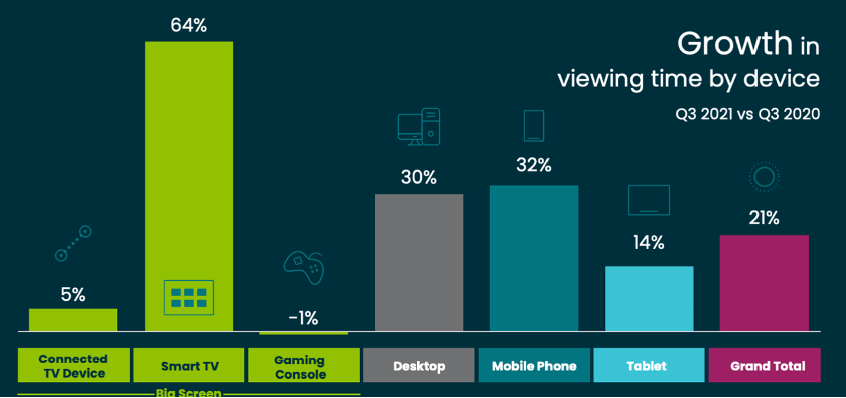

Moreover, reports from online video analytics company Conviva show that during every quarter of 2021, the global viewing time for CTV has grown as compared to 2020. For instance:

“According to Nielsen, in Q3 2021 ratings for adults 18-49 on traditional TV fell 19% y/y, creating supply shortages and increasing ad prices. As a result, the top 10 cable TV advertisers doubled spend on the Roku platform y/y. Total monetized video ad impressions nearly doubled year-over-year, driven by strong client acquisition and retention.” - Steve Louden, Roku’s CFO, January 2021

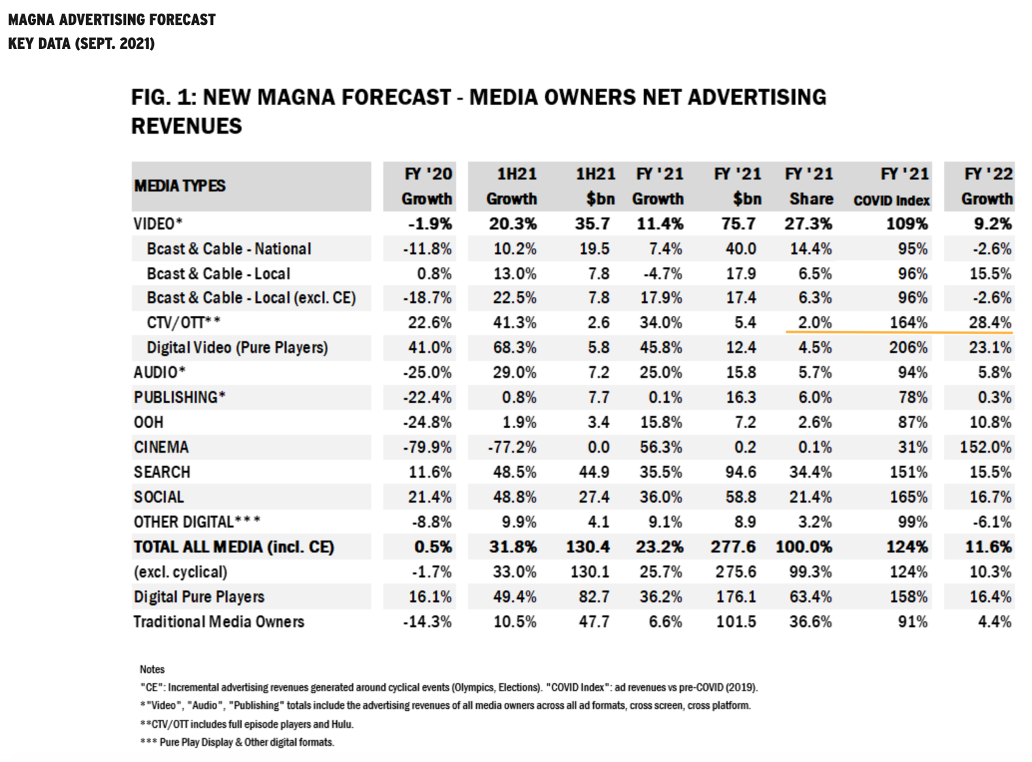

The Fastest Growing Video Advertising Platform Is Now CTV

In their latest ad spend study released in September 2021, IPG MAGNA, a media intelligence company was forecasting CTV ad spend to grow by 34% in 2021 totaling $5.4 billion for the year, making it the fastest growing video advertising platform.

For 2022, MAGNA is projecting continued growth with a year-over-year ad spend increase of 28.4% reaching nearly $7 billion in ad dollars:

A study done by The Trade Desk and Advertiser Perceptions which surveyed 150 advertisers, found that 92% of advertisers believe that CTV is as good as, or outperforms, linear TV advertising.

Their advertising budgets support this view, with 45% of advertising professionals increasing their CTV budgets over the last year. What’s more, among those who shifted budgets to CTV, 91% said they will maintain those shifts or increase investments in CTV.

How Much Does a TV Ad Cost?

The CTV advertising rates from CTV advertising companies are more costly than linear television impressions.

According to Keynes Digital, the median Cost-Per-Thousand (CPM) for broadcast/cable linear television ads is $10 to $15 CPM. The CPM for YouTube videos is $20 to $25, while the CPM for CTV ads is $35 to $65.

The justification for the much higher CTV ad cost is the difference in targeting options, that produces better cost performance, which results in a less-expensive Cost-Per-Completed-View (CPCV). Moreover, consumers completely view up to 95% of the CTV ads.

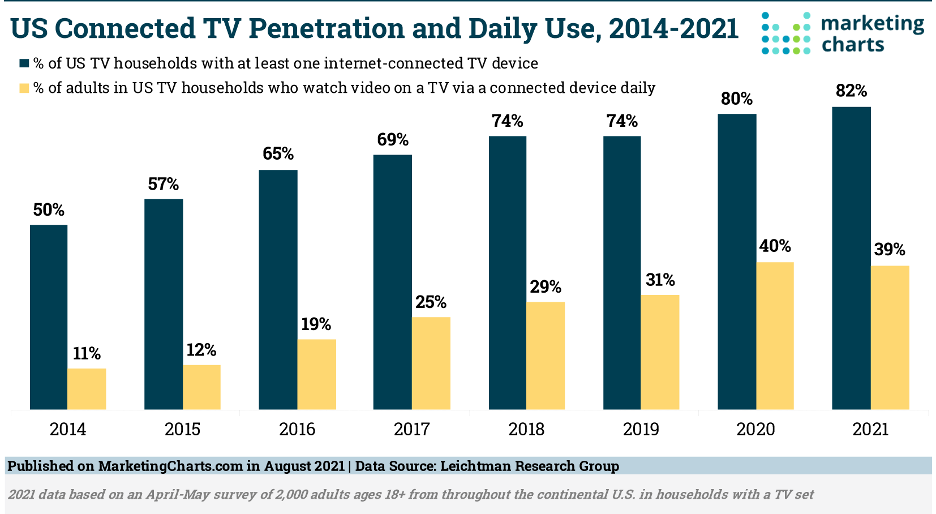

Almost 40% Of Adults Watch Video Daily On CTV, 60% Weekly

A survey done in the US in May 2021 shows that 39% of all adults watch video daily via a connected TV device, while 60% of adults watch video using a connected TV device at least once a week, compared to 59% in 2020. To no one’s surprise young adults are the heaviest viewers of CTV. This might be an indication that post-pandemic CTV viewing has not tailed off.

Moreover, 82% of U.S. TV households have at least one internet-connected TV device (this includes connected smart TVs sets or separate set-top-box devices, such as Roku, Amazon Fire TV, Chromecast, or Apple TV or connected video game systems).

57% of U.S. TV households had either Roku or Amazon Fire TV smart TVs or streaming devices in Q1 ’20, according to a survey in the newest Connected Home report. Out of the respondents, 40% of them owned a Roku while 29% owned an Amazon Fire TV or streaming device.

6. Competition

In terms of competition in the streaming OS space, it is undoubtedly fierce. Roku competes with much larger companies that have resources and brand recognition that pose significant competitive challenges.

The intense competition is a significant risk when investing in Roku’s shares. A short summary for the available CTVs / streaming devices:

Most recently, Google has made its “Google TV OS” a priority. Although the company already sells the Chromecast streaming device, which features the Android TV, Google has made significant efforts to have its newest software, the Google TV, already installed on connected TVs.

Besides its current exclusive manufacturing partners, like Japanese manufacturer Sony, Google is allegedly willing to pay hefty amounts to other Chinese TV manufacturers like TCL to install its software on connected devices (Google is willing to pay manufacturers from $10 to $15 per unit, compared to Roku’s $7 to $8 per unit fee).

As a result, TCL announced that it will now sell its top-notch connected TVs with both Roku and Android operating systems. ). So far TCL has been a long-term partner for Roku, selling their bundle of connected TVs and Roku OS for many years.

However, although this move takes away some of Roku’s competitive advantage, TCL has made it clear is not transitioning to Google TV instead of Roku or walking away from its longtime partner:

“TCL expects that the TV operating system landscape will take after smartphones and eventually consolidate down to two choices: Roku OS and Google TV”

Other huge established companies are following Google’s example, as Comcast launched in October 2021 its XClass TV, a new line of smart television sets built for streaming, powered by its Xfinity TV OS.

Amazon also announced in September 2021 its first ever Amazon-built smart TVs, the Amazon Fire TVs that feature hands-free voice control for Alexa at affordable prices.

Moreover, other manufacturers are also building their own OS for the CTV space. For instance, LG announced that more than 20 international TV manufacturers had already committed to its webOS partnership.

7. The Bear case

- competition from the more powerful and established players may be too much for Roku;

- creating its own content for TRC means Roku is entering another brutally competitive space filled with bigger and more experienced players: that of content creation; as a result, the company’s P&L might be seriously affected and the margins may shrink;

- growth in accounts active is already slowing;

- very small international presence, compared to its competitors;

- growth estimates are skewed because of the pandemic and Roku won’t be able to maintain the pace in the future;

- advertising spending shift from linear TV to streaming won’t happen at the pace that Roku anticipates;

8. Financial overview

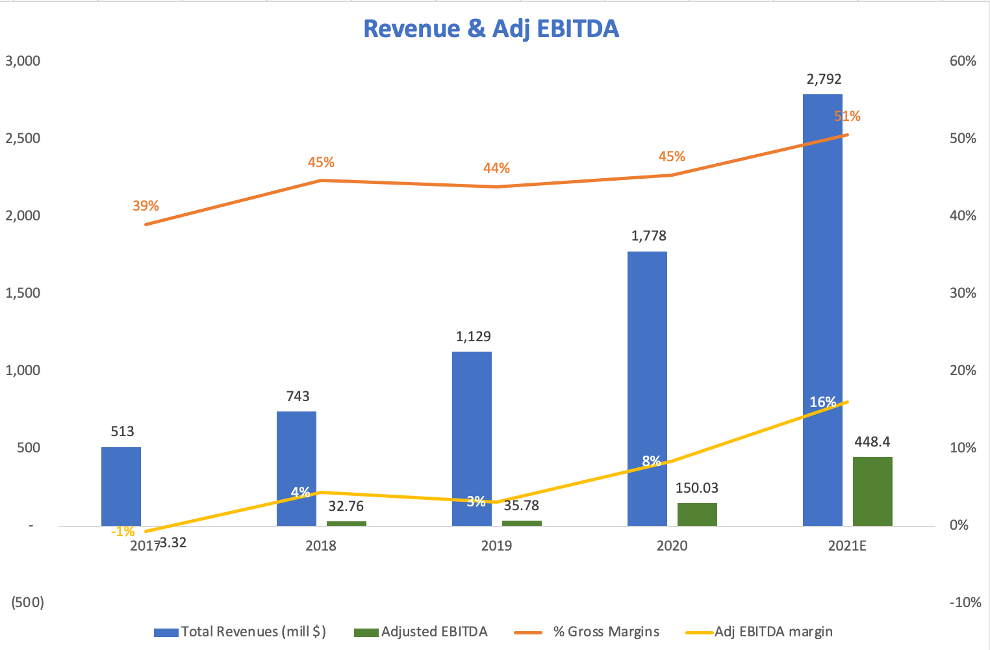

Revenue & Adjusted EBITDA

In terms of revenue, the business has growth significantly during the last couple of years. As we can see above, Roku grew its revenue with 57% in 2020, as the business benefited from the industry tailwinds generated by the COVID-19 pandemic. Moreover, the revenue growth expected for full year 2021 is also around 57%.

The gross profit has been consistent around 45% for the last couple of years, but this year it has crossed the 50% threshold.

We can also observe a major improvement in the adjusted EBITDA (which excludes stock-based compensation, depreciation and amortization) margin, which came at 8% in 2020 and is projected to double in 2021.

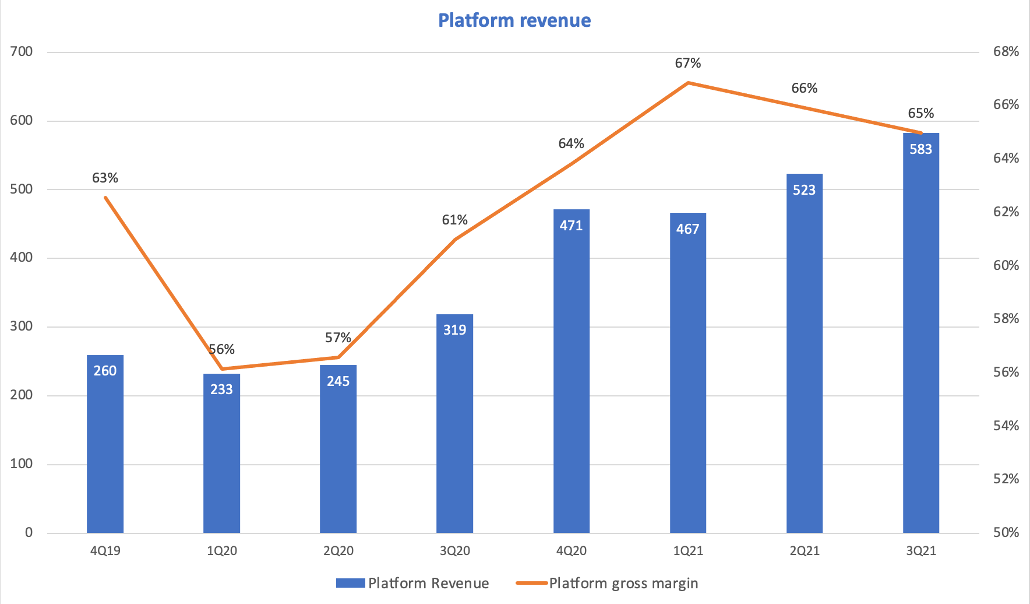

Platform vs Player

Giving the unique nature of Roku’s business, most of its revenue (~71% at the end of 2020) comes from platform revenue, while the player business is just the hardware component that’s actually a mean’s a means to an end, that of attracting users on the platform in order to monetize the activity via advertising.

As we can see below, the platform activity has been growing consistently while gross margin was improved and has been consistently above 65% for the last three quarters.

“Looking ahead at the player business, as a reminder, we do not optimize for player gross profit, but rather account growth.” - Steve Louden, Roku’s CFO, May 2021

Roku player unit sales remained above pre-COVID levels and the average selling price decreased 7% year-over-year as the company chose to insulate consumers from higher costs. They plan to do that in Q4 as well.

Player revenue and player unit sales were both down 26% year-over-year, following the pandemic-related demand spike in Q3 2020, but remained above pre-COVID levels in Q3 2019.

Going further on a quarterly level, we can see below the revenue growth trend, the major contribution of the Q4 and its significant growth YoY (37.5%). Moreover, in 3Q20 Roku has recorded a net profit for the first time since December 2018.

However, management offered a lackluster guidance for Q4 of 2021 in term of margins, indicating challenges created by the supply chain disruptions.

Management expects these headwinds to continue in 2022 as this was largely a function of lower inventory and higher component costs being passed along to consumers as overall U.S. TV prices increased 42% year-over-year. Also, US TV sales in Q3 fell below pre-COVID 2019 levels, down 31% y/y.

Balance Sheet

In term of balance sheet, we can observe the company has plenty of cash on its hand, but what’s really important here is the long-term debt and the number of shares outstanding. Roku has an insignificant amount of long-term debt so that’s not a risk for the investors:

However, the other aspect is the number of shares. Roku became a public company in Q3 2017, so compared with the end of 2017, the company has now 35% more stocks outstanding. In terms of compounded annual growth rate, this translates into a dilution of around 8% per year.

Although the 8% yearly dilution is not a very big percentage, shareholders must be aware of the potential risk of dilution.

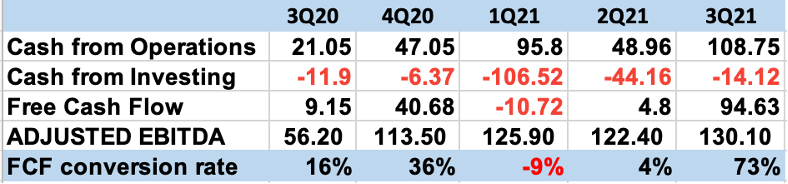

Another crucial aspect of every business is its capability of generating free cash-flow. The company has generated cash flow from operations for a long time and at the end of 2020 it generated free cash flow (FCF = Cash from operations – Capital expenditures) for the first time.

On a quarterly level, Roku has generated free cash flow starting with third quarter of 2020. The only exception was the first quarter of 2021.

One important metric that helps us see Roku’s ability to generate free cash is its FCF conversion rate:

The FCF conversion rate saw a major improvement in Q3 of 2021, but remains very volatile. The business is growing at a very fast pace and right now the management needs to capitalize on the market expansion opportunities and keep growing the business.

9. Valuation and technical

Valuation

In terms of valuation, Roku has experienced a major drop in its multiples. If we’re going to look at NTM (Next twelve months) Enterprise value / Revenue, Roku has a multiple around 7.5, which is lower than its 10.45 mean and around 70% lower than its highest value, of 26.9 achieved in February 2021.

Enterprise Value is a more accurate measure of the value of a firm, as it includes the debt, value of preferred shares and minority interest, but minus cash and cash equivalents.

When compared with some of its advertising peers, Roku seems to be still trading at a premium. However, please note this comparison contains many solid established companies that do not have as many growth opportunities as Roku:

Technical analysis

As any other growth stock, Roku stock has had a difficult 2021. After a tremendous run in 2020, the company reached its all-time high in February and then again in July, confirming the $480 area as a strong resistance:

We’ve seen recently a strong gap over the announcement that Roku and Google will continue their collaboration. However, since then we closed above the green candle and the stocks sits right at the anchored VWAP, starting with the lows from March 2020.

We saw some strong resistance levels around $265, but more important we can see that $200 support held very well on 2 occasions. I would of liked the stock to trade back to $170 (old resistance from 2019, possibly new support), but even around $200 the stock seems appealing.

Please also take into account the current macro environment and the uncertainty that is non-related to the company’s performance. I would like to see a couple of days/weeks of consolidation around the anchored VWAP or the $200 level since we got quickly rejected by the $265 resistance.

10. Conclusion

With its data measurement and analytics, Roku has tremendous potential to become one of the most dominant players in the advertising space and join the ranks of Google, Facebook or Amazon as an “walled garden” in the industry.

Given Roku’s recent pivot towards content creation, management must navigate that carefully so that margins won’t be affected. However, I trust the experienced management will take this task carefully and minimize the risk that this bold move brins with it.

If you feel like the streaming will become the dominant way of viewing TV and Roku will successfully defend its market share to the Amazons and Googles of the world, then Roku might be a good long-ter investment for your portfolio.

Disclosure: The article only expresses my opinion and it is NOT investment advice. Please do your own due diligence and only pick companies with your desired level of risk