Rare earth materials and the trend of electrification

Rare earth materials and the trend of electrification

Hi,

This is my 3rd write up and for this one I’m going to introduce a very special company. But this one is quite unique: it is not an exciting technology company or a tremendously innovative one. It is a boring company and all it does is mining. Why is this interesting for a potential investor? Because the materials they extract are virtually everywhere, more precisely inside permanent magnets.

The company is called MP Materials Inc. (“MP Materials” or “the company”), ticker symbol “MP”. In this write up I will detail why MP Materials is a company that pushes forward the electrification trend while strongly influencing the macroeconomic picture.

The industry

Before getting into the company specifics, I need to set the stage by defining some important talking points:

Firstly, a permanent magnet is an object that creates its own persistent magnetic field. Permanent magnets power the traction motors of electric vehicles (EVs), wind turbines, drones or robots amongst other important applications. While magnets have become a significant part of our technological development, I will be focusing more on the critical ingredients that originate in the magnets: rare-earth materials.

Rare-earth materials are a set of 17 chemical elements with special magnetic properties. They are considered rare because of the high cost of obtaining. The component that I’m going to focus on most during this newsletter is actually a mix of 2 rare elements: Neodymium and Praseodymium, forming Neodymium-Praseodymium (“NdPr”). It is a crucial element because it is the core material of high-strength permanent magnets.

The company

MP Materials owns and operates one of the world’s largest integrated rare earth mining and processing facilities in the world. Located in Mountain Pass, California, it is the only major rare earth resource in the Western Hemisphere with a proven, multi-decade reserve base.

A short background on the site:

The mine at Mount Pass has been used for about 70 years. The company that previously owned the Mount Pass was Molycorp. With a history of almost a century, Molycorp bought the usage rights for Mount pass in 2008 and in 2010 had its IPO. It had a similar mission to MP Materials, but unfortunately the company failed to execute on its vision and because of external factors like low prices for its minerals plus activating in a China dominated market, it crumbled and filed for bankruptcy in 2015.

Still, keep in mind that when Molycorp had its IPO the Tesla Model S wasn’t launched yet and the idea that electric vehicles will gain significant market share was still otherworldly. It seems like Molycorp might have existed ahead of its time.

As a result, Molycorp’s efforts led to an unexpected opportunity for MP Materials. Since Molycorp activated in California, the state regulations forced it to build state-of-the-art facilities that can operate an environmental friendly site. Since it failed to execute and after investing roughly 2 billion dollars and going bankrupt, the mine was bought by MP Materials who saw a way of fixing the imperfections and profit from it.

The process

MP materials operates in a special industry and hence it has created a three-stage plan to re-establish this critical industrial input within the United States. It is very important to note that every step of the plan is a different way of generating revenue:

Stage 1 – rare earth concentrate production

MP Materials currently operates at Mount Pass and mines a rare earth concentrate that represents 15% of the global supply. The concentrate is an intermediate product that is currently sold in Asia. As of now, MP’s median monthly production is 3.2 times bigger that of its predecessor.

Stage 2 – refining (separating the rare materials into individual oxides)

The company is currently building the biggest refining facility in the world. Refining is the next step after mining and can incur significant costs and expertise. The process allows to turn the intermediate product from stage 1 into separate rare earth materials at a significantly lower cost while utilizing environmental friendly procedures. The company believes it will start this process in 2022.

Stage 3 – production of NdPr magnets

Once stage 2 is finished, the company hopes to be able to produce NdPr magnets in the U.S. It is estimated that stage 3 will begin in 2025.

For the moment, after stage 1 is completed, the concentrated product is shipped to Asia. There it is refined, the NdPr is extracted and the permanent magnets are produced. Since the company doesn’t have the necessary technology in place for stage 2, it gives up a tremendous part of its potential profits while at the same time limiting its market. Their only market right now is China since the NdPr is not refined and MP materials can only sell to rare earth oxide producers. Once stage 2 is in place, the market will include any global producer of NdPr magnets (that are still only a handful, but more than the rare earth oxides producers).

The market

There is no doubt that the future of EVs is a crucial part of the puzzle. Today nobody knows for sure how the majority of vehicles will be powered in the future. Perhaps most of the motors will be powered by hydrogen batteries, lithium, cobalt or lithium-ion, but regardless of their powering option, all motors have permanent magnets as the dominant motor technology which translates into NdPr becoming the critical motor material.

In addition to the electric vehicles, the NdPr magnets market is much vaster. Here is a segmentation of the NdPr market as of 2019:

Investment thesis

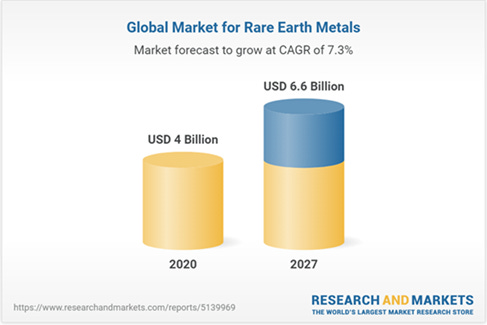

1. Rare-earth materials global market is expected to reach $6.6 billion by 2027, compared with $4 billion in 2020, growing at a CAGR of 7.3%. The US market alone was around $1.1 billion in 2020.

2. Electric vehicles (EVs) sales are soaring. The global electric vehicle market was valued at $162.34 billion in 2019, and it is projected to reach a staggering $802.81 billion by 2027, registering a CAGR of 22.6%.

3. U.S. president Joe Biden has recently announced the “Build back better”, which is a $2.2 trillion infrastructure plan that seeks to improve the U.S. transportation and semiconductor industry. This plan follows the signing of an executive order by the U.S. president to address chip shortage and to strengthen the supply chain:

The order includes a 100-day review of key products including semiconductors and advanced batteries used in electric vehicles, followed by a broader, long-term review of six sectors of the economy.

The infrastructure plan and the executive order signed by the U.S. president are immensely beneficial for MP Materials. The long-term plan is for the U.S. to quickly scale up processing and refining after the mining of the resources, and compete on a cost basis with the foreign magnet-makers. For the moment, it seems like this is a significant tailwind for MP Materials who must now execute proficiently.

The macroeconomic picture

So far we established that the key use for rare earth minerals is to build permanent magnets that are utilized for electric vehicles (EV), wind turbines, drones, basically every advanced motion technology. This includes numerous national defense equipment.

In 2019 China was responsible for 80% of rare earths imports in the US, according to the U.S. Geological Survey. This is a clear concern for the U.S. as shown in this 2018 report by the U.S. Department of Defense:

Areas of concern to America’s manufacturing and defense industrial base include a growing number of both widely used and specialized metals, alloys and other materials, including rare earths and permanent magnets.

These national concerns suggest that the success of MP Materials and other possible U.S. competitors might be critical for many U.S. industries and might play an important role in the geopolitical picture.

An important aspect of the mining process in the US is that California has very high environmental standards. Hence MP Materials is committed to becoming a sustainable low cost supplier of rare earth materials while also being held to some of the most stringent environmental standards.

Management team

James Litinsky is the CEO and chairman of MP Materials. Before acting as the CEO he was a hedge fund manager. While Molycorp was struggling with its execution and market pressure, he saw an opportunity and he stepped up to grab it. His investment firm bought the bonds issued by Molycorp in anticipation of it going bankrupt. Thereby James Litinsky’s firm bought Mountain Pass in 2017 for pennies on the dollar after a gruesome bankruptcy process and that’s how MP Materials was born.

Risks

- MP materials is a commodity based company. This means it is exposed to the same risks as other commodities, most notably to supply chain dynamics (i.e. market risk = prices can experience significant downswings).

However, it appears that for now the NdPr market is still in its infancy and it might take significant time and high costs in order to scale the supply to a point where it would exhaust the demand. Even with a big supply from China, all the catalysts indicate that we will have a contango market for the foreseeable future. Moreover, once stage 3 of MP’s plan will be running, the company expects to lower the NdPr pricing volatility since it will use its own raw material in order to create permanent magnets.

- Very limited market with the revenue coming 99% from a huge Chinese company. Even though MP Materials is a solid supplied to Shenghen Resoruces, the company remains exposed at least until stage 2 of its plan is started.

Competitors

In a market heavily dominated by China, MP Materials has 2 big outside of China competitors:

- Rare Element Resources – U.S. company focused on delivering strategic materials to technology industries by advancing plans to develop the Bear Lodge Critical Rare Earth Project, located in northeast Wyoming – no revenue yet for the company, still on the implementation stage

- Lynas Rare Earths – an Australian company that runs its own refining facility in Malaysia. It is the biggest competitor for MP Materials with approximately $300 million in revenue annually, while being the only company outside of China that can refine NdPr. However, the company has incurred some environmental challenges during the last couple of years and it has been forced by the Malaysian government to relocate its facility by 2023

Financials

Income Statement

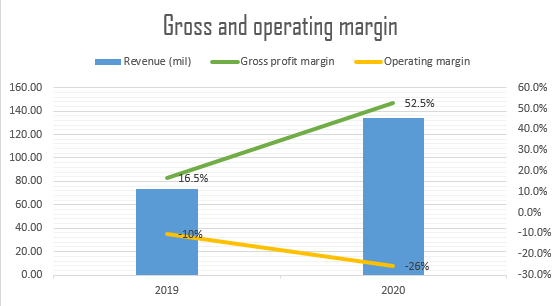

For full year 2020 the company registered a strong revenue growth – 83% YoY with a 100% revenue growth for Q4 of 2020 compared with the same period in 2019. More than 90% of MP Materials’ revenue comes from NdPr mining.

MP Materials is a unique business and has a niche market. As it can only sell to a few companies located in Asia, right now MP Materials sells 99% of its rare earth oxide to Chinese rare earths giant Shenghe Resources. So far the business looks as it follows:

As it can be seen above, the gross margin rose greatly, which is a good sign for the business. However, the operating margin has decreased because of a one-time $66.6 million non-cash settlement charge reflecting a deemed payment to terminate a “DMA” (a distribution and marketing agreement) signed with Shenghe Resources. The “DMA” was initially signed alongside other commercial agreements between MP materials and Shenghe Resources under which the latter pledges to offer know-how and funding for operating Mount Pass and in return it is entitled to a portion of the net profits from the sale of rare earth products extracted at the Mountain Pass in the subsequent years.

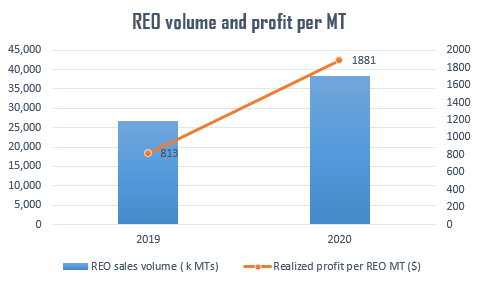

Besides the GAAP indicators, the company utilizes a few non-GAAP key performance indicators to assess the evolution of the business. They are concentrated around the volume of rare earth oxide (REO) that is sold during stage 1 and measured in MT (metric ton):

For the fiscal year 2020 we can see a definite improvement in the net dollar profit per MT as result of a 19% increase in the transaction price and a 28% drop in the production cost, which are great signs for the future of the company.

Cash flow statement

MP Materials has had positive cash flow from operations in 2020. This indicates that the business activity is sustainable and can generate free cash flow from operations, but as of now the company isn’t cash flow positive yet. Cash flow from financing was significant in 2020 since the company went public via a SPAC deal:

Valuation and technical

Now I did some digging and I found out that recently things got a little dicey for the shareholders. In March MP Materials announced the issuance of a $600 million green convertible bond with the opportunity for the institutional investors to buy more notes, up to $90 million. This note can be converted into cash or shares of common stock at a conversion price of around $44/share. If converted, the bond will acquire around 13.55 million shares of common stock which will lead to potential dilution for the existing shareholders.

However, even with the drawback following the issuance of the bond, MP Materials is still a pretty expensive stock. With a P/S around 37, it is more comparable with the P/S of a software company than a mining one. Because of this aspect, I would recommend caution when opening a position in MP Materials. Of course the fundamentals are strong, but even so they might be already priced-in. Here is a summary:

Following the selling of the bond and a generally short-term bearish trend in the markets, MP Materials has recently had a pull back. Right now it is traded around $32, but I do expect it to go a little lower in the future. As we can see below, the 28 area has acted as a recent support, but I do expect the stock to eventually intersect with the 200SMA on the daily chart (red line that is just forming). Here we have the daily chart:

Another interesting pattern that we can see forming on the daily chart is the 5 Elliot Waves pattern. It looks like we are in an ABC correction wave pattern. In order to make sure we can follow the lows around 27. If the 27 price will hold, it means we are in a ABC correction patter. Usually the B wave should not go lower than the 5th wave. After the ABC pattern unfolds it is possible that another bullish run will start. However, if the 27 short-term support breaks, the stock will probably go into its low 20s. Here we can see the pattern:

To sum up, following the price action closely and starting accumulating in important pivot points will go a long way, especially if long-term holding is desired. A drop under 27 would be a good opportunity for starting accumulating shares as long as the business fundamentals don’t deteriorate.

Conclusion

Mining rare earth elements is a truly unique business and the growing market needs a solid vendor that can supply high quality materials consistently. Once MP Materials will start refining its materials, it will set up the process of producing permanent magnets and possibly become a trusted western hemisphere supplier for the OEM industry.

This is definitely a long-term play. However, even if the firm runs a multi-year plan to meet investors’ expectations, the stock has been extremely volatile and might provide multiple entry opportunities as long as we remain patient.

Disclosure: The article only expresses my opinion and it is NOT investment advice. Please do your own due diligence and pick companies that have your desired level of risk